August 10, 2024 by Dan Mitchell @ International Liberty

Why do politicians such as Donald Trump and Kamala Harris show no interest in fixing Social Security and other entitlement programs?

The answer is “public choice.” They are focused on maximizing votes and power in the short run rather than doing what’s best for the country in the long run.

This is a pervasive problem and deserves its own theorem.

I’m motivated to share this new theorem because of a George Will column in the Washington Post.

But he’s not writing about fiscal policy. He has another example of how we get bigger problems because of short-term thinking by people in Washington.

With frequent references to Thomas Hoenig, the former head of the Kansas City Federal Reserve, he’s writing about bad monetary policy. Here are some excerpts.

How high will be the cost of interest rates, having been too low for too long? Events might be teaching a tutorial on the steep price of cheap money. …One purpose of the low rates was to send a flood of money into the increasingly frothy stock market… The Fed’s balance sheet of government and government-guaranteed assets, by which it nudges down interest rates, grew from $900 billion in 2007 to nearly $9 trillion in March 2022. …whenever the Fed has tried to “normalize its balance sheet and interest rates, the market has become unstable.” …

The question now…is will the Fed properly allow rates to come down only as inflation falls to the Fed’s 2 percent target, or will it aggressively try to fend off unwanted, but necessary, corrections — necessary for “better long-run outcomes?”

…Monday’s stock sell-off…ignited worried chatter about whether the Fed should have cut rates the week before, or might have to do so as an “emergency” measure before its scheduled meeting next month. This is not what panicky markets need: yet another government entity declaring yet another emergency.

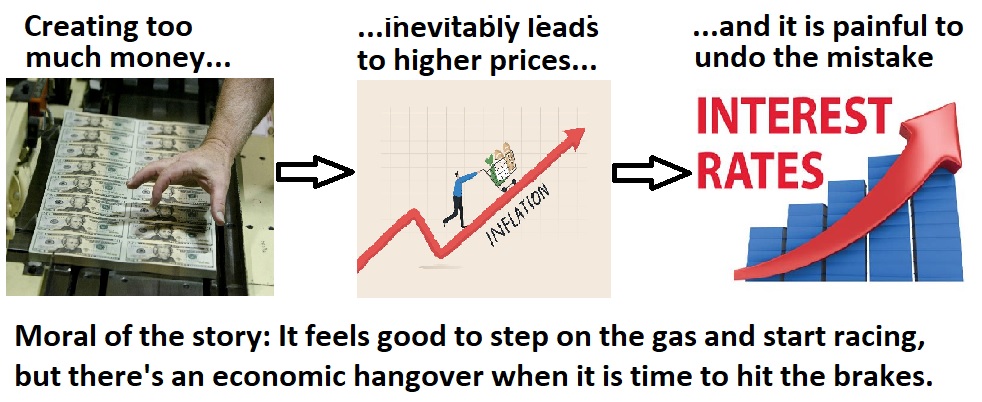

What Hoenig correctly worries about (and what George Will is writing about) is the problem of a boom-bust monetary policy.

Politicians like the sugar high the economy gets when the central bank creates excess money.

But that excess money creation inevitably causes bad things such as higher prices and asset bubbles.

The best thing is not to make the mistake in the first place. But if the mistake is made, the obvious solution is to “normalize” policy by withdrawing the excess money from the system.

However, this is painful in the short run, so politicians and the central bankers they appoint often don’t have the fortitude and integrity to do the right thing (Ronald Reagan was an exception to the rule).

I started this column with a fiscal policy example. I then cited a monetary policy example. Let’s now close with a bailout example.

Here’s a tweet making the point that propping up profligate nations is a recipe for more profligacy.

The tweet is about a central bank (the ECB) subsidizing bad behavior with bailouts, but it applies also to fiscal bailouts (like TARP) or international bureaucracy bailouts (like the IMF).

The bottom line is that bailouts produce moral hazard. Reward bad behavior and you get more bad behavior.

That make no sense, but politicians and their appointees are drawn to such policies because they want to minimize pain in the short run even though they are creating the conditions for far more pain in the long run.

P.S. Debt limit fights are an example of some people supporting short-run pain in order to reduce the likelihood of much greater long-run pain.

No comments:

Post a Comment