Thanks to the glorious miracle of capitalism, I’m writing this column 36,000 feet above the Atlantic Ocean.

I’m on my way back from Europe, where I ground through about a dozen presentations as part of a swing through 10 countries.

Most of my speeches were about the future of Europe, which was the theme of the Austrian Economic Center’s 2019 Free Market Road Show.

Most of my speeches were about the future of Europe, which was the theme of the Austrian Economic Center’s 2019 Free Market Road Show.

So it was bad timing that I didn’t have a chance until now to comb through a new study from three scholars about the economic impact of the European Union. As they point out at the start of their research, EU officials clearly want people to believe European-wide governance is a recipe for stronger growth.

It seems that the European Union has not triggered or enabled better economic performance.

So EU countries should be catching up to America.

Yet the opposite is happening. Here’s the relevant chart on US vs. EU performance.

The scholars conducted various statistical tests.

Many of those test actually showed that EU membership is associated with weaker performance.

Last but not least, the authors compared former Soviet Bloc nations to see if linking up with the EU led to improvements in economic performance.

These are not flattering results.

Here’s a look at the relevant chart.

These findings leave me with a feeling of guilt. For almost twenty years, I’ve been telling audiences in Eastern Europe that they probably should join the EU.

Yes, I realized that meant a lot of pointless red tape from Brussels, but I always assumed that those costs would be acceptable because the EU would give them expanded trade and help improve the rule of law.

I’ll have to do some thinking about this issue before my next trip.

P.S. In case you’re wondering why I’ve been telling Eastern European nations to join the EU while telling the United Kingdom to go for a Clean Brexit, my analysis (at least up til now) has been that market-oriented nations are held back by being in EU while poorer and more statist economies are improved by EU membership.

I’m on my way back from Europe, where I ground through about a dozen presentations as part of a swing through 10 countries.

Most of my speeches were about the future of Europe, which was the theme of the Austrian Economic Center’s 2019 Free Market Road Show.So it was bad timing that I didn’t have a chance until now to comb through a new study from three scholars about the economic impact of the European Union. As they point out at the start of their research, EU officials clearly want people to believe European-wide governance is a recipe for stronger growth.

Here’s a bit of background on their methodology.The great European postwar statesmen, including the EU founding fathers, clearly…envisaged the establishment of a common political and economic entity as a guarantor of…domestic economic progress. …Article 2 of the foundational Treaty of Rome explicitly talked about “raising the standard of living.” … in practice EU today mainly emphasizes growth, as is evident from its most ambitious recent policy agendas. In 2000, a stated aim of the Lisbon Agenda was to make the European economy the “most competitive and knowledge-based economy in the world, capable of sustainable economic growth with more and better jobs and greater social cohesion.” And all seven of the Flagship Initiatives adopted as part of the Europe 2020 Strategy were about growth—smart, sustainable, and inclusive.

…the focus of the present paper will be on prosperity as the key outcome that the EU will be measured up against… Our approach in the present paper is to use different empirical strategies (difference-in-differences type setups and standard growth regressions); slice the length of the panel in various ways (e.g., dropping post crisis observations); look at different samples of countries (e.g., a global sample, the sample of original OECD countries, the sample of formerly planned economies, and the sample of EU member countries); pay attention to spatial dependencies; and, finally, require manipulability of the treatment variable.And what did they find?

It seems that the European Union has not triggered or enabled better economic performance.

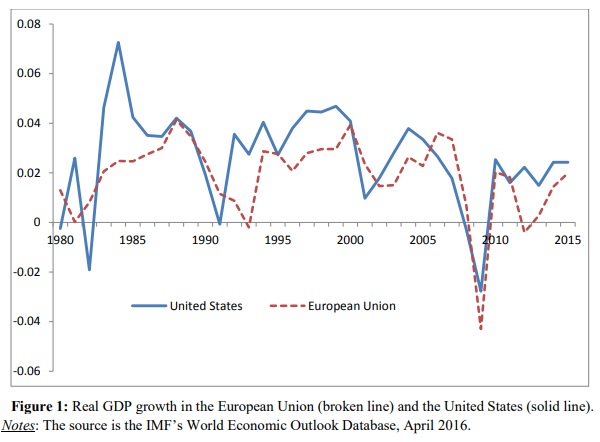

The conclusion that emerges upon looking systematically at the data is that EU membership has no impact on economic growth. …We start by simply looking at the comparative performance of the EU and the United States, which is the comparison that Niall Ferguson makes. The IMF’s World Economic Outlook Database provides real GDP growth rates going back to 1980 for the EU and the US. These are plotted in Figure 1. The EU only managed to outperform the US economy in terms of real GDP growth in ten out of the 35 years between 1980 and 2015. …With these growth rates, the US economy would double its size every 27 years, whereas the corresponding number for the EU is 36 years. This hardly amounts to stellar performance on part of the EU.What makes this data so remarkable is that convergence theory tells us that poorer nations should grow faster than richer nations.

So EU countries should be catching up to America.

Yet the opposite is happening. Here’s the relevant chart on US vs. EU performance.

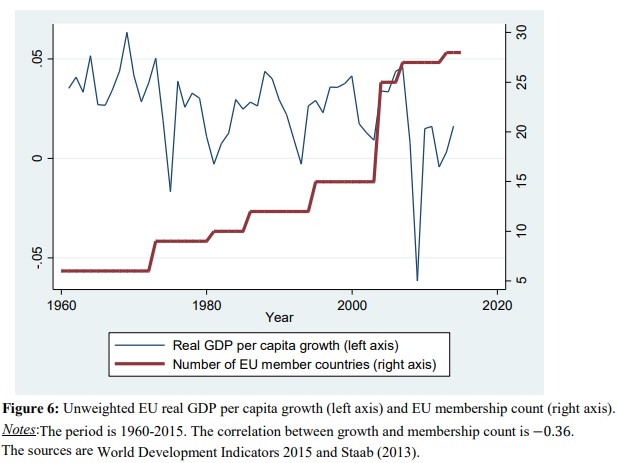

The scholars conducted various statistical tests.

Many of those test actually showed that EU membership is associated with weaker performance.

…we basically measure pre- and post-entry growth for the EU countries up against the growth trajectories of all other countries. …EU membership is associated with lower economic growth in all columns. …where we use the maximum length WDI sample (i.e., 1961-2015), EU entry is associated with a statistically significant growth reduction of roughly 1.8 percentage points per year. When we remove the period associated with the sovereign debt crisis in the Eurozone (i.e., 2010-15), the reduction remains significant but is lower (1.27 percentage points per year). Finally, when we remove the global financial crisis of 2008-09, the reduction (which is now statistically insignificant) is 0.5 percentage points per year. Using GDP per worker growth from PWT gives roughly similar results… Consequently, in a difference-in-differences type setting EU entry seems to have reduced economic growth.Moreover, a bigger EU (i.e., more member nations) is associated with slower average growth.

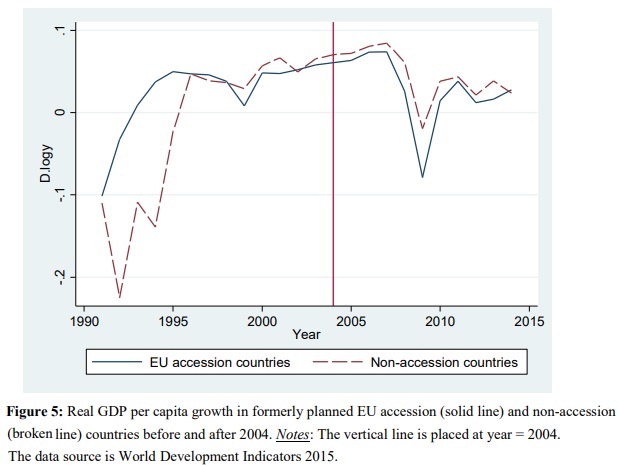

Last but not least, the authors compared former Soviet Bloc nations to see if linking up with the EU led to improvements in economic performance.

…we ask whether growth picked up in the new Eastern European EU countries after accession vis-à-vis growth in 18 formerly planned non-EU countries. …Of the 11 accession countries, not a single one had higher average annual real GDP per capita growth in the period after the EU accession as compared to the period before.Ouch.

These are not flattering results.

Here’s a look at the relevant chart.

These findings leave me with a feeling of guilt. For almost twenty years, I’ve been telling audiences in Eastern Europe that they probably should join the EU.

Yes, I realized that meant a lot of pointless red tape from Brussels, but I always assumed that those costs would be acceptable because the EU would give them expanded trade and help improve the rule of law.

I’ll have to do some thinking about this issue before my next trip.

P.S. In case you’re wondering why I’ve been telling Eastern European nations to join the EU while telling the United Kingdom to go for a Clean Brexit, my analysis (at least up til now) has been that market-oriented nations are held back by being in EU while poorer and more statist economies are improved by EU membership.

No comments:

Post a Comment