There’s general agreement among public finance experts that personal income taxes and corporate income taxes, on a per-dollar-collected basis, do the most economic damage.

And I suspect there’s a lot of agreement that this is because these levies often have high marginal tax rates and often are accompanied by a significant bias against income that is saved and invested.

Payroll tax and consumption taxes, by contrast, are thought to be less damaging because they generally don’t have “progressive rates” and they are “neutral,” meaning they rarely involve any double taxation of saving and investment.

But “less damaging” is not the same as “no damage.”

Such taxes still drive a wedge between pre-tax income and post-tax consumption, so they do result in less economic activity (what economists refer to as “deadweight loss“).

And the deadweight loss can be significant if the overall tax burden is sufficiently onerous (as is the case in many European nations).

Interestingly, the (normally pro-tax) International Monetary Fund just released a study on this topic. It looked at the impact of taxes on work in the new member states (NMS) of the European Union. Here’s a summary of what the authors wanted to investigate.

So the personal and corporate income taxes are not a major burden.

But they so have relatively high payroll taxes (a.k.a., social insurance taxes) and relatively onerous value-added taxes.

So it’s hardly a surprise that these levies are the ones most associated with deadweight loss.

And here’s an explanation of what it means.

And here’s some of the explanatory text.

And it’s good that an IMF report is providing good evidence for lower tax rates.

But I’m not optimistic we’ll get pro-growth changes. There’s been a lack of good reform this decade from the new member states from Eastern Europe. Combined with demographic decline (and the associated pressure for higher tax rates), this does not bode well.

P.S. While the professional economists at the IMF often produce good research and sensible advice, the bureaucracy’s political leaders almost always ignore those findings and instead push for bad tax policy. Including in the new member states from Eastern Europe.

And I suspect there’s a lot of agreement that this is because these levies often have high marginal tax rates and often are accompanied by a significant bias against income that is saved and invested.

Payroll tax and consumption taxes, by contrast, are thought to be less damaging because they generally don’t have “progressive rates” and they are “neutral,” meaning they rarely involve any double taxation of saving and investment.

But “less damaging” is not the same as “no damage.”

Such taxes still drive a wedge between pre-tax income and post-tax consumption, so they do result in less economic activity (what economists refer to as “deadweight loss“).

And the deadweight loss can be significant if the overall tax burden is sufficiently onerous (as is the case in many European nations).

Interestingly, the (normally pro-tax) International Monetary Fund just released a study on this topic. It looked at the impact of taxes on work in the new member states (NMS) of the European Union. Here’s a summary of what the authors wanted to investigate.

Given demographic and pension pressures facing many EU28 countries amidst low labor market participation rates together with still high tax wedges, the call to review public policies has gained renewed prominence in the EU political debate. …tax wedges remain high and participation rates, while having increased importantly in a few countries over 2000-17 , are still around or below 70 percent in many of them. This hints at the need for addressing structural problems to improve economic fortunes. In this paper we focus our attention on hours worked (per working age population). …At country level, hours worked reflect labor supply decisions and could be thought of a measure of labor utilization. Long-run changes in labor supply are driven by incentives, of which taxes are perceived to be central. Assessing the importance of taxation on hours is key to provide new insights for potential policy actions.And here’s what they found.

We study the role of taxes in accounting for differences in hours worked across NMS over the 1995-17 period… We find that consumption and labor taxes significantly discourage labor supply and can explain close to 21 percent of the observed variation of hours across NMS. …Higher tax rates reduce households’ net labor income and real purchasing power, inducing them to substitute consumption for leisure, which cannot be taxed. …Our findings show that, conditional on other factors, taxes are an important determinant of hours. Point estimates suggest a high elasticity of hours to taxes (close to 0.5), which is robust to the inclusion of other factors.What’s interesting about the new member states of Eastern Europe is that many of them have flat taxes and low corporate rates.

So the personal and corporate income taxes are not a major burden.

But they so have relatively high payroll taxes (a.k.a., social insurance taxes) and relatively onerous value-added taxes.

So it’s hardly a surprise that these levies are the ones most associated with deadweight loss.

We find that social security contributions deter hours the most, followed by consumption taxes and, to a lesser extent, personal income taxes. …Consumption and personal income taxes are found to affect hours per worker, but not employment rates. On the other hand, social security contributions are negatively associated with employment rates, but do not seem to affect hours per worker. …In line with the literature, we document that women’s employment rate is more sensitive to changes in tax policies. We find the elasticity of employment rate to social security contributions to be 7 percent larger for women vis-à-vis men.Here’s one of the charts from the study.

And here’s an explanation of what it means.

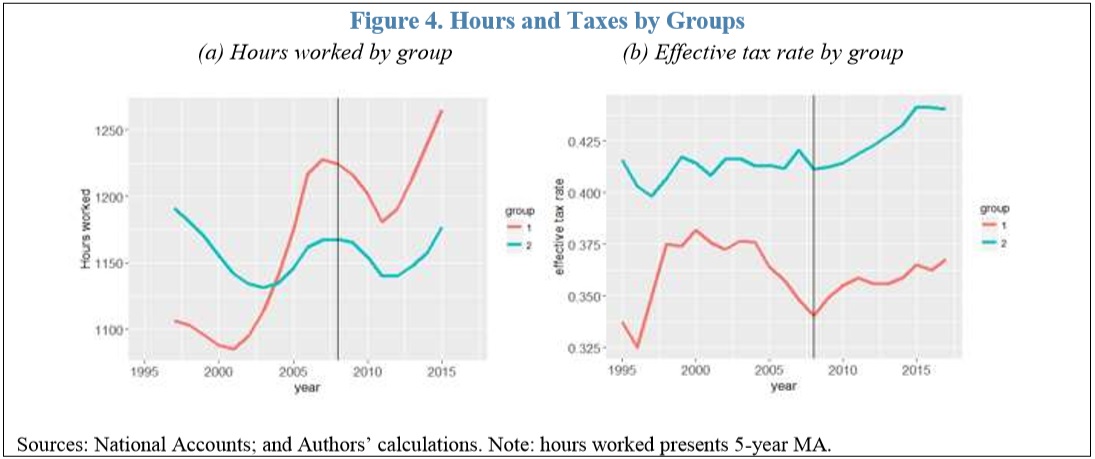

Figure 4 shows the evolution of hours and effective taxes. Hours worked increased substantially for Group 1, while it remained stable in Group 2 (Panel (a)). In both groups, the effect of the GFC is noticeable as hours sharply declined after 2008. Panel (b) shows the evolution of the average effective tax rate in each group. Interestingly, countries in Group 1, which observed an increase in hours, had lower effective tax rates (below 40 percent) throughout the period. In addition, we observe a negative correlation between hours and taxes for most of the sample. For Group 1, the large increase in hours – between year 2000 and the GFC – happened at the same time taxes declinedHere’s another chart from the IMF report.

And here’s some of the explanatory text.

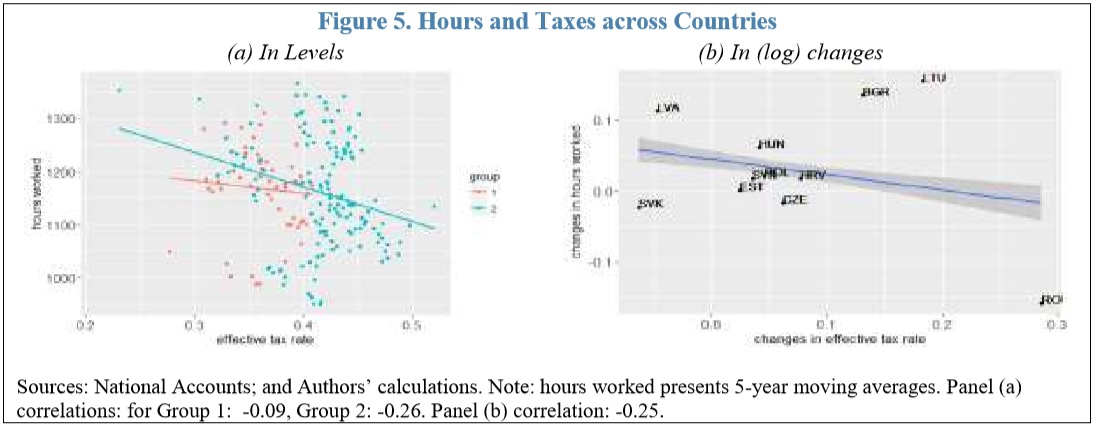

Figure 5 depicts the relationship between hours worked and taxes across countries. In Panel (a), we observe a negative correlation between hours and taxes in levels for each group, with the negative correlation being stronger in Group 2 than in Group 1 (it has a steeper slope). Panel (b) shows total log changes in hours and taxes throughout the period. It also displays a negative correlation.Looking at the conclusion, a key takeaway from the study is that there is a substantial loss of economic activity because of theoretically benign (but in reality onerous) taxes on consumption and labor.

Our modelling exercise shows that taxes influence the long-run trend in hours and our econometric exercise shows that the findings are robust to the inclusion of other labor market determinants. Furthermore, we document an elasticity of hours to overall taxes close to 0.5. We find that differences in tax burden can explain up to 21 percent in the variation of hours worked across NMS. The main takeaway of this study is that excessive tax burden, either in the form of consumption or labor taxes, can lead to substantial deadweight losses in terms of labor supply. .. overall tax burden – and not only labor taxes – should be considered when thinking about incentives from tax schemes.Yes, incentives do matter.

And it’s good that an IMF report is providing good evidence for lower tax rates.

But I’m not optimistic we’ll get pro-growth changes. There’s been a lack of good reform this decade from the new member states from Eastern Europe. Combined with demographic decline (and the associated pressure for higher tax rates), this does not bode well.

P.S. While the professional economists at the IMF often produce good research and sensible advice, the bureaucracy’s political leaders almost always ignore those findings and instead push for bad tax policy. Including in the new member states from Eastern Europe.

No comments:

Post a Comment