Given Social Security’s enormous long-run financial problems, the program eventually will need reform.

But what should be done? Some folks on the left, such as Barack Obama and Hillary Clinton, support huge tax increases to prop up the program. Such an approach would have a very negative impact on the economy and, because of built-in demographic changes, would merely delay the program’s bankruptcy.

But what should be done? Some folks on the left, such as Barack Obama and Hillary Clinton, support huge tax increases to prop up the program. Such an approach would have a very negative impact on the economy and, because of built-in demographic changes, would merely delay the program’s bankruptcy.

Others want a combination of tax increases and benefit cuts. This pay-more-get-less approach is somewhat more rational, but it means that today’s workers would get a really bad deal from Social Security.

This is why I frequently point out that personal retirement accounts (i.e., a “funded” system based on real savings) are the best long-run solution. And to help the crowd in Washington understand why this is the best approach, I explain that dozens of nations already have adopted this type of reform. And I’ve written about the good results in some of these jurisdictions.

Now it’s time to add Sweden to the list.

I actually first wrote about the Swedish reform almost 20 years ago, in a study for the Heritage Foundation co-authored with an expert from Sweden. Here’s some of what we said about the nation’s partial privatization.

I’m a big fan of the fully privatized portion of the Swedish system (the “premium pension”) funded by the 2.5 percent of payroll that goes to personal accounts.

But let’s first highlight the very good reform of the government’s portion of the retirement system. It’s still a tax-and-transfer scheme, but there are “notional” accounts, which means that benefits for retirees are now tied to how much they work and how much they pay into the system.

A new study for the American Enterprise Institute, authored by James Capretta, explains the benefits of this approach.

Now let’s look at some background on the privatized portion of the new system. Here’s a good explanation in a working paper from the Center for Fiscal Studies at Sweden’s Uppsala University.

Let’s close by citing another passage from Capretta’s AEI study.

He looks at Sweden’s long-run fiscal outlook to other major European economies.

And the fiscal burden of Sweden’s system could fall even more if lawmakers allowed workers to shift a greater share of their payroll taxes to personal accounts.

But any journey begins with a first step. Sweden moved in the right direction. The United States could learn from that successful experience.

P.S. Pension reform is just the tip of the iceberg. As I wrote two years ago, Sweden has implemented a wide range of pro-market reforms over the past few decades, including some very impressive spending restraint in the 1990s. If you’re interested in more information about these changes, check out Lotta Moberg’s video and Johan Norberg’s video.

But what should be done? Some folks on the left, such as Barack Obama and Hillary Clinton, support huge tax increases to prop up the program. Such an approach would have a very negative impact on the economy and, because of built-in demographic changes, would merely delay the program’s bankruptcy.Others want a combination of tax increases and benefit cuts. This pay-more-get-less approach is somewhat more rational, but it means that today’s workers would get a really bad deal from Social Security.

This is why I frequently point out that personal retirement accounts (i.e., a “funded” system based on real savings) are the best long-run solution. And to help the crowd in Washington understand why this is the best approach, I explain that dozens of nations already have adopted this type of reform. And I’ve written about the good results in some of these jurisdictions.

Now it’s time to add Sweden to the list.

I actually first wrote about the Swedish reform almost 20 years ago, in a study for the Heritage Foundation co-authored with an expert from Sweden. Here’s some of what we said about the nation’s partial privatization.

While that study holds up very well, let’s look at more recent research so we can see how the Swedish system has performed.Swedish policymakers decided that both individual workers and the overall economy would benefit if the old-age system were partially privatized. …Workers can invest 2.5 percentage points of the 18.5 percent of their income that they must set aside for retirement. …the larger part-16 percent of payroll-goes to the government portion of the program. …What makes the government pay-as-you-go portion of the pension program unique, however, is the formula used for calculating an individual’s future retirement benefits. Each worker’s 16 percent payroll tax is credited to an individual account, although the accounts are notional. …the government uses the money in these notional accounts to calculate an annuity (annual retirement benefit) for the worker. …the longer a worker stays in the workforce, the larger the annuity received. This reform is expected to discourage workers from retiring early… There are many benefits to Sweden’s new system, including greater incentives to work, increased national savings, a flexible retirement age, lower taxes and less government spending.

I’m a big fan of the fully privatized portion of the Swedish system (the “premium pension”) funded by the 2.5 percent of payroll that goes to personal accounts.

But let’s first highlight the very good reform of the government’s portion of the retirement system. It’s still a tax-and-transfer scheme, but there are “notional” accounts, which means that benefits for retirees are now tied to how much they work and how much they pay into the system.

A new study for the American Enterprise Institute, authored by James Capretta, explains the benefits of this approach.

The final part of the above excerpts is key. The system automatically adjusts, thus presumably averting the danger of future tax hikes.Sweden enacted a reform of its public pension system that combines a defined-contribution approach with a traditional pay-as-you-go financing structure. The new system includes better work incentives and is more transparent to participants. It is also permanently solvent due to provisions that automatically adjust payouts based on shifting demographic and economic factors. …A primary objective…in Sweden was to build a new system that would be solvent permanently within a fixed overall contribution rate. …pension benefits are calculated based on notional accounts, which are credited with 16.0 percent of workers’ creditable wages. …The pensions workers get in retirement are tied directly to the amount of contributions they make to the system. …This design improved incentives for work… To keep the system in balance, this rate of return is subject to adjustment, to correct for shifts in demographic and economic factors that affect what rate of return can be paid within the fixed budget constraint of a 16.0 percent contribution rate.

Now let’s look at some background on the privatized portion of the new system. Here’s a good explanation in a working paper from the Center for Fiscal Studies at Sweden’s Uppsala University.

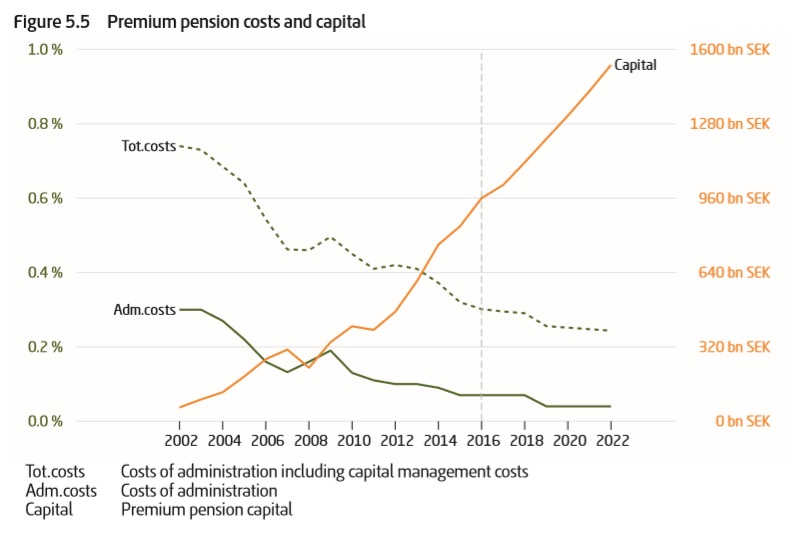

And here’s a chart from the Swedish Pension Agency’s annual report showing that pension assets are growing rapidly (right axis), in part because “premium pension has provided a 6.7 percent average value increase in people’s pensions per year since its launch.” Moreover, administrative costs (left axis) are continuously falling. Both trends are very good news for workers.The Premium Pension was created mainly for three purposes. Firstly, funded individual accounts were believed to increase overall savings in Sweden. …Secondly, the policy makers wanted to allow participants to take account of the higher return in the capital markets as well as to tailor part of their pension to their risk preferences. Finally, an FDC scheme is inherently immune against financial instability, as an individual’s pension benefit is directly financed by her past accumulated contributions. The first investment selections in the Premium Pension plan took place in the fall of 2000, which is known as the “Big Bang” in Sweden’s financial sector. …any fund company licensed to do business in Sweden is allowed to participate in the system, but must first sign a contract with the Swedish Pensions Agency that specifies reporting requirements and the fee structure. Benefits in the Premium Pension Plan are paid out annually and can be withdrawn from age 61.

Let’s close by citing another passage from Capretta’s AEI study.

He looks at Sweden’s long-run fiscal outlook to other major European economies.

According to European Union projections, Sweden’s total public pension obligations will equal 7.5 percent of GDP in 2060, which is a substantial reduction from the…8.9 percent of GDP it spent in 2013. …In 2060, EU countries are expected to spend 11.2 percent of GDP on pensions. Germany’s public pension spending is projected to increase…to 12.7 percent of GDP in 2060. …The EU forecast shows France’s pension obligations will be 12.1 percent of GDP in 2060 and Italy’s will be 13.8 percent of GDP.I think 8.9 percent of GDP is still far too high, but it’s better than diverting 11 percent, 12 percent, or 13 percent of economic output to pensions.

And the fiscal burden of Sweden’s system could fall even more if lawmakers allowed workers to shift a greater share of their payroll taxes to personal accounts.

But any journey begins with a first step. Sweden moved in the right direction. The United States could learn from that successful experience.

P.S. Pension reform is just the tip of the iceberg. As I wrote two years ago, Sweden has implemented a wide range of pro-market reforms over the past few decades, including some very impressive spending restraint in the 1990s. If you’re interested in more information about these changes, check out Lotta Moberg’s video and Johan Norberg’s video.

No comments:

Post a Comment