Writing a column every day can sometimes be a challenge, in part because of logistics (I have to travel a lot, which can make things complicated), but also because I want to make sure I’m sharing interesting and relevant information.

My task, however, is very easy on certain days. When Economic Freedom of the World is published in the autumn, I know that will be my topic (as it was in 2017, 2016, 2015, etc). My only challenge is to figure out how to keep the column to a manageable size since there’s always so much fascinating data.

Likewise, I know that I have a very easy column about this time of year (2017, 2016, 2015, etc) since that’s when the Social Security Administration releases the annual Trustees Report.

It’s an easy column to write, but it’s also depressing since my main goal is to explain that the program already consumes an enormous pile of money and that it will become an every bigger burden in the future.

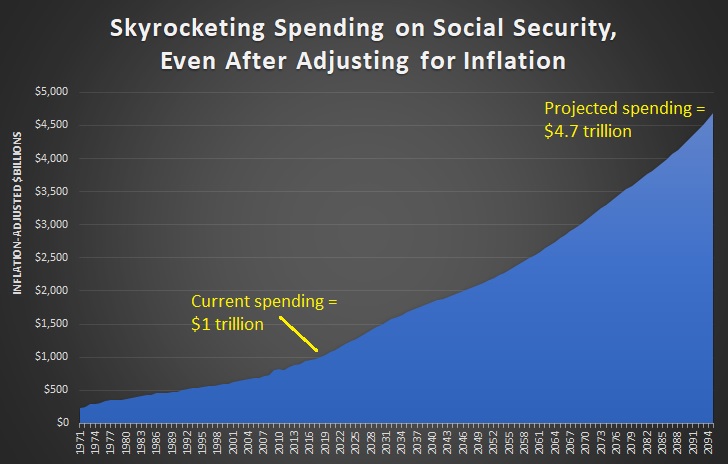

Here are the 1970-2095 budgetary outlays from the latest report, adjusted for inflation. As you can see, the forecast shows a huge increase in spending.

The good news, as least relatively speaking, is that we’ll also have inflation-adjusted growth between now and 2095, so the numbers aren’t quite as horrifying as they appear. That being said, Social Security inexorably will consume a larger share of the private economy over time.

Now let’s examine a second issue. Most news reports incorrectly focus on the year the Social Security Trust Fund runs out of money.

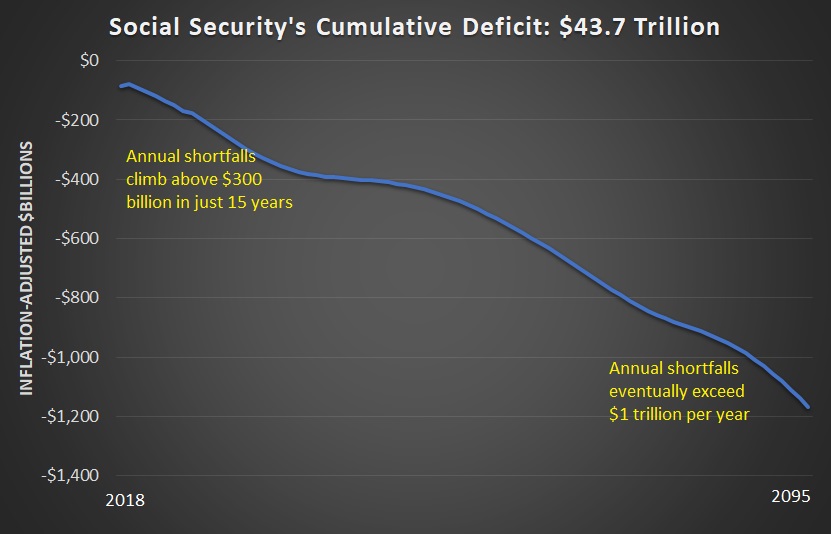

But since that “Trust Fund” is filled with nothing but IOUs, I think that’s an utterly pointless piece of data. So every year I show the cumulative $43.7 trillion cash-flow deficit in the system. Using inflation-adjusted dollars, of course.

Assuming we don’t reform the program, think of these numbers as a reflection of a built-in future tax hike.

You won’t be surprised to learn, by the way, that politicians such as Barack Obama and Hillary Clinton already have identified their preferred tax hikes to fill this gap.

Let’s wrap up.

Veronique de Rugy of Mercatus accurately summarizes both the problem and the solution.

Veronique explains we need to reform the system by allowing personal retirement accounts. She was even kind enough to quote me cheerleading for the Australian system.

The bottom line is that there’s been a worldwide revolution in favor of private savings and the United States is falling behind.

P.S. If you have some statist friends and family who get confused by numbers, here’s a set of cartoons that shows the need for Social Security reform.

P.P.S. As I explain in this video, reform does not mean reducing benefits for current retirees, or even older workers.

My task, however, is very easy on certain days. When Economic Freedom of the World is published in the autumn, I know that will be my topic (as it was in 2017, 2016, 2015, etc). My only challenge is to figure out how to keep the column to a manageable size since there’s always so much fascinating data.

Likewise, I know that I have a very easy column about this time of year (2017, 2016, 2015, etc) since that’s when the Social Security Administration releases the annual Trustees Report.

It’s an easy column to write, but it’s also depressing since my main goal is to explain that the program already consumes an enormous pile of money and that it will become an every bigger burden in the future.

Here are the 1970-2095 budgetary outlays from the latest report, adjusted for inflation. As you can see, the forecast shows a huge increase in spending.

The good news, as least relatively speaking, is that we’ll also have inflation-adjusted growth between now and 2095, so the numbers aren’t quite as horrifying as they appear. That being said, Social Security inexorably will consume a larger share of the private economy over time.

Now let’s examine a second issue. Most news reports incorrectly focus on the year the Social Security Trust Fund runs out of money.

But since that “Trust Fund” is filled with nothing but IOUs, I think that’s an utterly pointless piece of data. So every year I show the cumulative $43.7 trillion cash-flow deficit in the system. Using inflation-adjusted dollars, of course.

Assuming we don’t reform the program, think of these numbers as a reflection of a built-in future tax hike.

You won’t be surprised to learn, by the way, that politicians such as Barack Obama and Hillary Clinton already have identified their preferred tax hikes to fill this gap.

Let’s wrap up.

Veronique de Rugy of Mercatus accurately summarizes both the problem and the solution.

Veronique punctures the myth that there’s a “Trust Fund” that can be used to magically pay benefits.The single largest government program in the United States will soon have an annual budget of $1 trillion a year. …The program is Social Security, and our national pastime seems to be turning a blind eye to its dysfunctions. …Since 2010, it has been running a cash-flow deficit—meaning that the Social Security payroll taxes the government collects aren’t enough to cover the benefits it’s obliged to pay out. …

Prior to 2010, the program collected more in payroll taxes than was needed to pay the benefits due at the time. The leftovers were “invested” into Treasury bonds through the so-called Old Age Trust Fund, which is now being drawn down. …In fact, the Treasury bonds are nothing but IOUs. …Treasury…doesn’t have the money: It has already spent it on wars, roads, education, domestic spying, and much more. So when Social Security shows up with its IOUs, Treasury has to borrow to pay the bonds back. …Did you catch that? Past generations of workers paid extra payroll taxes to bulk up the Social Security system. But the government spent that additional revenue on non-retirement activities, so now your children and grandchildren will also have to pay more in taxes to reimburse the program.So what’s the solution?

Veronique explains we need to reform the system by allowing personal retirement accounts. She was even kind enough to quote me cheerleading for the Australian system.

Congress should shift away from Social Security into a “funded” system based on real savings, much as Australia and others have done. The libertarian economist Daniel J. Mitchell notes that, starting in the ’80s and ’90s, that country has required workers to put 9.5 percent of their income into a personal retirement account. As a safety net—but not as a default—Australians with limited savings are guaranteed a basic pension. That program has generated big increases in wealth. Meanwhile, Social Security has generated big deficits and discouraged private saving. Who would you have emulate the other?Though I’m ecumenical. I also have written favorably about the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system. Heck, I even like the system in the Faroe Islands.

The bottom line is that there’s been a worldwide revolution in favor of private savings and the United States is falling behind.

P.S. If you have some statist friends and family who get confused by numbers, here’s a set of cartoons that shows the need for Social Security reform.

P.P.S. As I explain in this video, reform does not mean reducing benefits for current retirees, or even older workers.

No comments:

Post a Comment