August 25, 2020 by

Dan Mitchell @ International Liberty

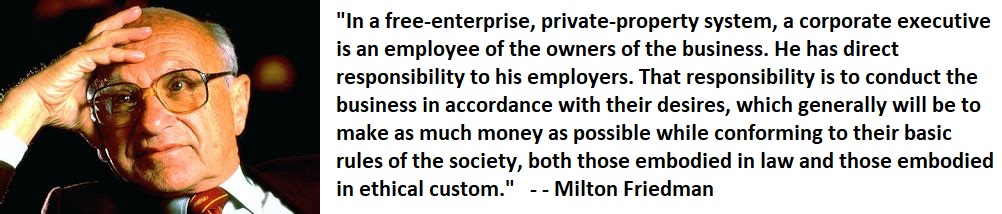

Milton Friedman was one of the the 20th century’s greatest defenders of capitalism and individual freedom. He had marvelous insights on issues such as

fiscal policy,

Sweden,

tax competition, and

other people’s money, but one of my favorite Friedman quotes is about the role of business.

This should be non-controversial, but

we need to remember that big companies are

not necessarily strong proponents of free enterprise. Yes, they like lower tax rates and a few other market-oriented policies, but many large firms are

more than happy to

climb into bed with big government so they can

gain special advantage from subsidies, handouts, bailouts, and protectionism. So we shouldn’t be surprised to learn that the trade association for corporate CEOs of

has disavowed Friedman.

Business Roundtable is modernizing its principles on the

role of a corporation. Since 1978, Business Roundtable has periodically

issued Principles of Corporate Governance that include language on the

purpose of a corporation. Each version of that document issued since

1997

has stated that corporations exist principally to serve their

shareholders. …We therefore provide the following Statement on the

Purpose of a Corporation, which supersedes previous Business Roundtable

statements and more accurately reflects our commitment… This statement

represents only one element of Business Roundtable’s work to ensure more

inclusive prosperity.

Business Roundtable is modernizing its principles on the

role of a corporation. Since 1978, Business Roundtable has periodically

issued Principles of Corporate Governance that include language on the

purpose of a corporation. Each version of that document issued since

1997

has stated that corporations exist principally to serve their

shareholders. …We therefore provide the following Statement on the

Purpose of a Corporation, which supersedes previous Business Roundtable

statements and more accurately reflects our commitment… This statement

represents only one element of Business Roundtable’s work to ensure more

inclusive prosperity.

You can read the new language

here. There’s only one pages of text and you’ll notice that it’s a lot of vapid jargon without any measurable commitments. Indeed, the letter is so vague that some observers think it’s irrelevant. In

a column for the

Washington Post,

James Copland of the Manhattan Institute points out that

profit-maximizing companies already consider the interests of so-called

stakeholders.

Critics and

supporters of business alike have characterized the statement as a major

shift away from “shareholder” capitalism toward an alternative

“stakeholder” model pushed by some progressive academics and

policymakers. It isn’t.

Critics and

supporters of business alike have characterized the statement as a major

shift away from “shareholder” capitalism toward an alternative

“stakeholder” model pushed by some progressive academics and

policymakers. It isn’t.

The Business Roundtable’s statement

unequivocally states that “the free-market system is the best means of

generating good jobs, a strong and sustainable economy, innovation, a

healthy environment and economic opportunity for all.”

To be sure, it proclaims that each of the chief executives signing on

shares “a fundamental commitment to all of our stakeholders” — including

customers, suppliers, employees and the broader community. But that’s a

truism. No business can long survive without meeting such stakeholders’

needs. …The corporate signatories do not suggest in any way weakening

the fiduciary duties of the boards and managers of ordinary for-profit

shareholder corporations to manage such companies’ affairs for

shareholders’ benefit.

…there is a big difference between saying that a

for-profit shareholder corporation should be sensitive to varying

constituencies’ concerns and saying that its principal purpose is

something different from the traditional view. One needn’t be an expert

in public-choice economics or corporate governance to understand that

politicizing corporate decision-making would be inefficient.

Lucian Bebchuk and

Roberto Tallarita of Harvard Law School, in

a column for the

Wall Street Journal, share some real-world evidence that the CEOs are engaging in empty posturing.

Although the Roundtable described the statement as a

radical departure from shareholder primacy, observers have been debating

whether it signaled a significant shift in how business operates or was

a mere public-relations move. …

Although the Roundtable described the statement as a

radical departure from shareholder primacy, observers have been debating

whether it signaled a significant shift in how business operates or was

a mere public-relations move. …

We contacted the companies whose CEOs

signed the Business Roundtable statement and asked who was the

highest-level decision maker to

approve the decision. Of the 48 companies that responded, only one said

the decision was approved by the board of directors. …The most

plausible explanation for the lack of board approval is that CEOs didn’t

regard the statement as a commitment to make a major change in how

their companies treat stakeholders. …

a review of the board-approved

corporate governance guidelines of the companies whose CEOs joined the

statement…mostly reflect a clear “shareholder primacy” approach. …The

evidence is clear: Notwithstanding statements to the contrary, corporate

leaders are generally still focused on shareholder value.

I think these two columns are accurate. The vast majority of the CEOs who signed the Business Roundtable’s

letter presumably have no intention of making unprofitable decisions

solely to curry favor with the broader community. That being said, the letter is still bad news because it basically acquiesces to the left’s

misguided view that profits are somehow bad for society. The

Wall Street Journal made this point in an

editorial in defense of the Friedman position.

The mucky-mucks of the Business Roundtable are tweeting

in unison how “proud” they are to have abandoned the corporate purpose

of serving shareholders for the more politically au courant

“stakeholder” model. …media cheerleaders seem especially pleased that

the CEOs have thrown the late, great economist Milton Friedman over the

side.

…The attempt to smear Friedman’s counsel as amoral is false. His point

was that profitable businesses serve the common good better than

executives who spend money on “social responsibility” but preside over

business failure. The second point is Friedman’s warning that CEOs who

put social responsibility above shareholders will find it redounds to

their detriment. They feed the public belief that free markets and

business are “wicked and immoral” and must be curbed by “external

forces,” which typically means politicians.

The mucky-mucks of the Business Roundtable are tweeting

in unison how “proud” they are to have abandoned the corporate purpose

of serving shareholders for the more politically au courant

“stakeholder” model. …media cheerleaders seem especially pleased that

the CEOs have thrown the late, great economist Milton Friedman over the

side.

…The attempt to smear Friedman’s counsel as amoral is false. His point

was that profitable businesses serve the common good better than

executives who spend money on “social responsibility” but preside over

business failure. The second point is Friedman’s warning that CEOs who

put social responsibility above shareholders will find it redounds to

their detriment. They feed the public belief that free markets and

business are “wicked and immoral” and must be curbed by “external

forces,” which typically means politicians.

In

a column for

National Review, Andrew Stuttaford also fears that the letter gives a green light to those who want more regulation by government.

The executives who retool a company’s mission to suit a

particular conception of “social responsibility” are spending

shareholders’ money on a moral agenda… Often repackaged as a demand that

corporations be measured by the extent to which they match arbitrary

and ever-tightening E (environmental), S (social), and G (governance)

standards, it

is now a way of corralling private enterprise without the bother of

legislation. …

The executives who retool a company’s mission to suit a

particular conception of “social responsibility” are spending

shareholders’ money on a moral agenda… Often repackaged as a demand that

corporations be measured by the extent to which they match arbitrary

and ever-tightening E (environmental), S (social), and G (governance)

standards, it

is now a way of corralling private enterprise without the bother of

legislation. …

the flourishing (and profitable) ecosystem that ESG

investing has created…encompasses consultancies, advocacy organizations,

“chief sustainability officers,” and many, many more rent-seekers

besides. ESG is bad news for investors, but it is not a bad way of

filling the wallets of those that feed off it. …

In effect, therefore,

many companies…will be forced to change the way they do business as they

try to keep up with ever-more-stringent rules set not by democratically

elected legislators but by the unaccountable, the ambitious, the

greedy, and the fanatical.

Speaking of unaccountable and greedy, that’s a good description of

Elizabeth Warren’s legislation to give Washington greater control of major companies. Professor Greg Mankiw of Harvard

opined about this issue last month for the

New York Times.

If you open any standard economics textbook, such as one

of mine, you will be told that a firm’s objective is to maximize profit.

…Given the vast range of economic and political problems the world

faces, this approach is often said to be too narrow....former Vice

President Joseph R. Biden Jr.,…joined in the criticism.

If you open any standard economics textbook, such as one

of mine, you will be told that a firm’s objective is to maximize profit.

…Given the vast range of economic and political problems the world

faces, this approach is often said to be too narrow....former Vice

President Joseph R. Biden Jr.,…joined in the criticism.

“It’s way past

time we put an end to the era of shareholder capitalism, the idea the

only responsibility a corporation has is with shareholders…

They have a responsibility to their workers, their community, to their

country.” …In forsaking a mandate of narrow self-interest for one of

broad social welfare, this approach to corporate management sounds

noble, perhaps even obvious. But it is more problematic under closer

scrutiny. …this approach to corporate management expects executives to

be broadly competent social planners rather than narrowly focused profit

maximizers.

It’s unlikely that corporate executives, with their

business training and limited experience, have the skills to play this

role well. …One lesson of Econ 101 is that the self-interested behavior

of consumers and businesses, directed by market forces and constrained

by competition, can lead to desirable outcomes.

In

an op-ed

earlier this year for the Wall Street Journal, Vivek Ramaswamy opined

that he and his fellow CEOs should not have a special role in

determining economic policy.

‘Stakeholder capitalism” is…the fashionable notion that

companies should serve not only their shareholders, but also other

interests and society at large. …

‘Stakeholder capitalism” is…the fashionable notion that

companies should serve not only their shareholders, but also other

interests and society at large. …

My main problem with stakeholder

capitalism is that it strengthens the link between democracy and

capitalism at a time when we should instead disentangle one from the

other. …Managers of corporations gain their positions by maximizing

profits and minimizing losses. …But

these business leaders have no special standing to decide whether a

minimum wage for American workers is more important than full

employment, or whether minimizing society’s carbon footprint is more

important than raising prices on consumer goods. …

I have no special

standing to legislate my morals because I am a CEO. I do, however, make

the final decision about our company’s research-and-development budget.

…the reason many corporate executives are speaking up in favor of

stakeholder capitalism is that they think they will gain popularity at a

time when it is unpopular to be perceived as a pure capitalist. …

Some

may argue that companies will be more successful in serving shareholders

over the long run if they also serve societal interests. If that’s

true, then classical capitalism should do the job, since only companies

that serve society will ultimately thrive, and “stakeholder capitalism”

would be superfluous.

But some CEOs can’t resist the temptation. The

Wall Street Journal opined about the social-justice posturing of one of the the CEOs who signed the Business Roundtable’s letter.

BlackRock CEO Larry Fink…has assumed a role as

self-styled conscience of the business world in telling CEOs how to run

their companies. …BlackRock is the world’s largest asset manager, with

some $7.43 trillion in client assets.

BlackRock CEO Larry Fink…has assumed a role as

self-styled conscience of the business world in telling CEOs how to run

their companies. …BlackRock is the world’s largest asset manager, with

some $7.43 trillion in client assets.

He is now threatening to vote

against corporate directors and management if they don’t do what he

says, and he is especially exercised about climate change.

…Corporations in which BlackRock invests will also have to comply with

the rules from a “Sustainability Accounting Standards Board” on issues

such as labor practices and workforce diversity.

…Like his friends at

the Business Roundtable, Mr. Fink is big on “stakeholder” capitalism.

…If he means serving employees, customers, suppliers and communities, he

is merely saying what any successful company already does. But our

guess is that by stakeholders Mr. Fink really means regulators and

politicians. …We can’t help but wonder if Mr. Fink, after a profitable

life in business, is auditioning to be Treasury Secretary.

In

an article

for the Foundation for Economic Education, Professor T. Norman Van Cott

makes the all-important point that successful companies automatically

generate benefits for people other than shareholders.

The marketplace is an arena where buyers and sellers both win. Do buyers and sellers really

care about each other? …I sure am grateful that I don’t have to depend

on the good-heartedness of Florida orange producers to send oranges to

Indiana.

The marketplace is an arena where buyers and sellers both win. Do buyers and sellers really

care about each other? …I sure am grateful that I don’t have to depend

on the good-heartedness of Florida orange producers to send oranges to

Indiana.

It’s not that the orange producers and I aren’t well-meaning, just

that oranges would not find their way to Indiana if good-heartedness

were the motivation for commerce.

…Microsoft provides a wonderful

example…the shareholder value of Microsoft, as large as it is, surely

pales in comparison to what its customers around the world gain.

…Microsoft has achieved its immense shareholder value not because its

customers, workers, suppliers, and communities are poorer. Indeed,

nothing could be further from the truth. Its stakeholders have been

enriched immeasurably by its pursuit of maximum shareholder value.

Writing for

USA Today, Professor Steve Hanke is

very critical of the Business Roundtable.

…the Business Roundtable launched a major attack

on property rights, the bedrock of capitalism. …the Roundtable, which

represents nearly 200 of America’s blue-chip companies, downgraded

shareholders.

…the Business Roundtable launched a major attack

on property rights, the bedrock of capitalism. …the Roundtable, which

represents nearly 200 of America’s blue-chip companies, downgraded

shareholders.

According to the Roundtable, the purpose of a corporation

will no longer be to conduct business with the sole objective of

generating profits for shareholders.

Owners of corporations (read: shareholders) will now just be one of

five “stakeholders”… The Roundtable’s new anti-capitalist mission

statement promises to dilute and muffle shareholders’ voices and further

politicize corporate governance. …

The great Austrian economist Joseph

Schumpeter concluded in his 1942 classic “Capitalism, Socialism and

Democracy” that businessmen would “never put up a fight under the flag

of their own ideals and interest.” …Schumpeter concluded that

businessmen, through their ignorance and cowardice, would assist those

who wished to destroy capitalism.

Megan McArdle also is skeptical. Here’s some of what

she wrote for the

Washington Post.

…business

leaders have no right to do charity on someone else’s dime. You might

admire plumbers who donate fixtures to needy families, but not if they

donated the fixtures you’d purchased for your own bathroom. That is

essentially what stakeholder capitalists are demanding of chief

executives: Take the money and power that shareholders have entrusted to

you and divert those resources to benefit someone else.

…business

leaders have no right to do charity on someone else’s dime. You might

admire plumbers who donate fixtures to needy families, but not if they

donated the fixtures you’d purchased for your own bathroom. That is

essentially what stakeholder capitalists are demanding of chief

executives: Take the money and power that shareholders have entrusted to

you and divert those resources to benefit someone else.

…if “stakeholder capitalism” means anything, it must mean companies

doing things that make shareholders at least somewhat worse off.

…Corporate social responsibility…can be even less accountable than good

old-fashioned shareholder capitalism. Money is relatively easy to

measure: Shareholders have more of it at the end of the quarter, or they

don’t, and either way you know how the boss is doing.

But if the chief

executive pours that cash into better-upholstered offices, more-generous

fringe benefits and a slew of charitable causes, who’s to say whether

the company’s goals are being met? …As Harvard health-care economist

Amitabh Chandra noted on Twitter after the Business Roundtable’s

announcement, “appealing to an amorphous ‘social mission’ ” has allowed

nonprofit hospitals “to foil regulators, acquire their competition, and

increase market power.” Beware of any proposal that might make the rest

of the economy look more like the health-care sector.

Robert Samuelson’s

column in the

Washington Post points out that previous episodes of “corporate social responsibility” did not yield good outcomes.

…we’ve already

been here. In the first decades after World War II, large U.S.

corporations adopted a social and political model very much like the

model recommended by the Roundtable.

…we’ve already

been here. In the first decades after World War II, large U.S.

corporations adopted a social and political model very much like the

model recommended by the Roundtable.

There was much talk of

“stakeholders,” not shareholders. Companies were supposed to attend to

their social responsibilities.

“Capitalism” as a term went out of style… The corporate responsibility

fad of the 1950s and 1960s was premised on the belief that…companies

could achieve both their traditional financial goals as well as the less

traditional agenda of providing higher living standards and employment

security. …

What we know with hindsight is that this confidence was a

conceit of a moment in time. …These lessons of history have been either

forgotten or ignored. But they have not gone away. Rather than heap

endless new responsibilities on companies, we’d be better off having

them tend to their traditional tasks — including maximizing profits.

By the way, the problem of big business rejecting capitalism isn’t limited to the CEOs of the Business Roundtable. Writing for

Project Syndicate, Klaus Schwab of the World Economic Forum (the folks who put on the Davos conference for the establishment’s high flyers)

argues for a middle ground between free markets and Chinese-style cronyism.

What kind of capitalism do we want? …we have three models

to choose from. The first is “shareholder capitalism,” embraced by most

Western corporations, which holds that a corporation’s primary goal

should be to maximize its profits.

What kind of capitalism do we want? …we have three models

to choose from. The first is “shareholder capitalism,” embraced by most

Western corporations, which holds that a corporation’s primary goal

should be to maximize its profits.

The second model is “state

capitalism,” which entrusts the government with setting the direction of

the economy, and has risen to prominence in many emerging markets, not

least China.

…the third has the most to recommend it. “Stakeholder capitalism,” a

model I first proposed a half-century ago, positions private

corporations as trustees of society… We should seize this moment…

To

that end, the World Economic Forum is releasing a new “Davos Manifesto,”

which states that companies should pay their fair share of taxes, show

zero tolerance for corruption, uphold human rights throughout their

global supply chains, and advocate for a competitive level playing

field…a new measure of “shared value creation” should include

“environmental, social, and governance” (ESG) goals as a complement to

standard financial metrics. …

Business leaders now have an incredible

opportunity. By giving stakeholder capitalism concrete meaning, they can

move beyond their legal obligations and uphold their duty to society.

Given that per-capita living standards are

much lower in China

than they are in the United States, I’m baffled that Schwab thinks it’s

a good idea to move halfway toward the decrepit Chinese model of

cronyism and

industrial policy. Does he think that people in North America and Western Europe should only be twice as rich as people in China

instead of four-to-six times richer? Let’s wrap up. The president of the Business Roundtable just wrote

a one-year anniversary review of his group’s campaign for so-called stakeholder capitalism.

It’s been a year since 181 CEOs of America’s largest

companies overturned a 22-year-old policy statement that defined a

corporation’s principal purpose as maximizing shareholder return.

…

It’s been a year since 181 CEOs of America’s largest

companies overturned a 22-year-old policy statement that defined a

corporation’s principal purpose as maximizing shareholder return.

…

Companies have held to their commitments. …many Roundtable companies

were making substantial investments in worker training, better wages and

benefits,

and support for struggling communities. They called for increases in

the federal minimum wage and paid family medical leave. …

In recent

weeks, CEOs have made new commitments to promote racial equality and

diversity in their own companies. …Far from undermining shareholders or

capitalism, the many actions major corporations are taking to support

all stakeholders will pay dividends… Business Roundtable CEOs

reject…quick-hit, short-term capitalism. They agree with many of the

nation’s largest investors that the health of both companies and

capitalism depends on investments in all stakeholders.

Sounds very noble and caring, at least for the folks who don’t understand economics. Which is why I almost laughed out loud when I saw

this tweet, which is based on

this article published by the

Atlantic.

The Roundtable is trying to curry favor with statists, but some folks

on the left are smart enough to see that it’s all empty posturing.

So what’s my contribution to this debate? Most of what I would say is captured in the excerpts above. Simply stated, it’s

not a good idea to mix big business with big government. But I will take this opportunity to unveil another one of my theorems.

P.S. Back in 2012,

I criticized the Business Roundtable for embracing tax increases on small businesses, so you can see that the Eleventh Theorem of Government is way overdue.

P.P.S. You can peruse the other ten theorems of government by

clicking here.