When I put forth the “The Case for Social Security Personal Accounts” in early 2011, I pointed out that the program’s long-run fiscal shortfall was more than $27 trillion.

We should be so lucky to have that problem today.

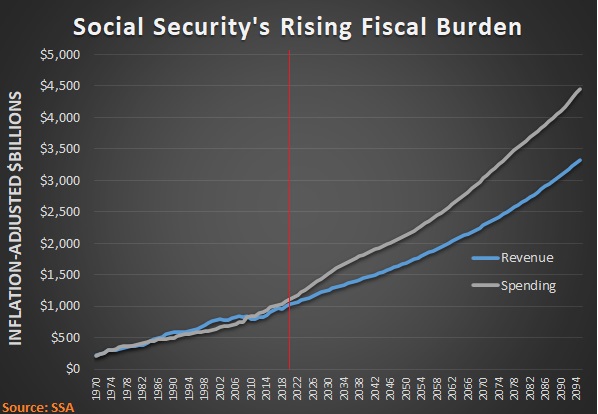

The Social Security Administration just released the annual report on the program’s finances, so I went to to Table VI.G9 of the “Supplemental Single-Year Tables” to peruse the yearly projections for future revenue and spending (which are adjusted for inflation so we have a more accurate method for comparisons).

The bad news is that an ever-increasing amount of our income is going to be grabbed by payroll taxes. The worse news is that Social Security’s spending burden will climb at an even-faster rate (historical data to the left of the red line, future projections to the right of the red line).

For those who focus on the less-important issue of red ink, the gap between revenue and spending over the next 75 years is projected to reach $44.7 trillion.

The gap in this year’s report is not directly comparable to the number I cited in 2011, but there’s no question the program’s finances are heading in the wrong direction.

This is partly because Social Security – as a “pay-as-you-go” program – is very vulnerable to demographic changes.

Like other types of Ponzi Schemes, it can work so long as there are always more and more new people entering the system.

But America’s demographic profile is changing. We’re living longer and having fewer kids.

In a column for the Foundation for Economic Education, Daniel Kowalski has a summary of how the program works and why it has a grim future.

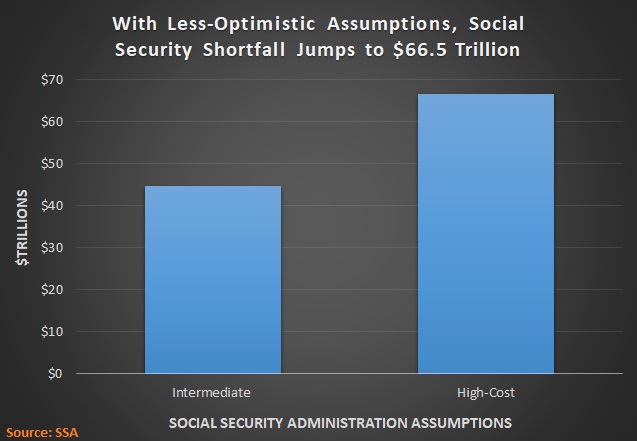

By the way, the numbers in the two charts above are based on the Social Security Administration’s “intermediate” assumptions.

I’ve never had any reason to question the reasonableness of those numbers. But in a world with coronavirus, which is causing crippling short-run economic damage and could cause significant long-run harm, it may be more prudent to look at SSA’s “high-cost” assumptions.

The bottom line is that the program’s long-run shortfall could be more than $20 trillion higher.

And remember, these numbers are in 2020 dollars. In other words, adjusted for inflation.

So how do we solve this mess? How do we avoid a grim fiscal future?

Shifting to a system of personal retirement accounts would be the most prudent approach. Yes, there would be an enormous transition cost since we would need to pay benefits to current retirees and many older workers, but that transition cost would be less than the $44.7 trillion unfunded liability (or even more!) of the current system.

I’ve written many times about the benefits of personal accounts for the United States, but I find most people are more interested in real-world evidence. Here are just a few of the several dozen nations that either fully or partially utilize private savings instead of political promises.

P.S. Some folks in Washington want to exacerbate Social Security’s fiscal burden by expanding the program.

P.P.S. I hate to add to the bad news, but the long-run finances for Medicare and Medicaid are an even-bigger problem.

We should be so lucky to have that problem today.

The Social Security Administration just released the annual report on the program’s finances, so I went to to Table VI.G9 of the “Supplemental Single-Year Tables” to peruse the yearly projections for future revenue and spending (which are adjusted for inflation so we have a more accurate method for comparisons).

The bad news is that an ever-increasing amount of our income is going to be grabbed by payroll taxes. The worse news is that Social Security’s spending burden will climb at an even-faster rate (historical data to the left of the red line, future projections to the right of the red line).

For those who focus on the less-important issue of red ink, the gap between revenue and spending over the next 75 years is projected to reach $44.7 trillion.

The gap in this year’s report is not directly comparable to the number I cited in 2011, but there’s no question the program’s finances are heading in the wrong direction.

This is partly because Social Security – as a “pay-as-you-go” program – is very vulnerable to demographic changes.

Like other types of Ponzi Schemes, it can work so long as there are always more and more new people entering the system.

But America’s demographic profile is changing. We’re living longer and having fewer kids.

In a column for the Foundation for Economic Education, Daniel Kowalski has a summary of how the program works and why it has a grim future.

He’s right, and his column doesn’t even address the other problem for young people, which is the fact that they get a rotten deal from the program, paying in record amounts of money in exchange for hollow promises of a meager monthly benefit.Social Security recipients are not paid with the money that the government deducted directly from them and their past employers. Instead that money was used to pay the benefits for past retirees, while current retired recipients are getting their money through Americans who are currently working and contributing to the system. …the first recipients of the Social Security program took out far more than they put in with the difference being made up by the fact that active workers then greatly outnumbered beneficiaries. In 1940 this was not an issue as there were 159 workers supporting one beneficiary. …By 1960, 15 years after President Roosevelt’s death, that ratio was reduced to 5 workers for every beneficiary. In 1980, the ratio dropped to just above three and in 2010 it dropped below that. …there is one thing that Millennials and Generation Z can do to prepare themselves for that day. Start saving and planning for retirement now and make a plan that does not count on a government-issued Social Security check.

By the way, the numbers in the two charts above are based on the Social Security Administration’s “intermediate” assumptions.

I’ve never had any reason to question the reasonableness of those numbers. But in a world with coronavirus, which is causing crippling short-run economic damage and could cause significant long-run harm, it may be more prudent to look at SSA’s “high-cost” assumptions.

The bottom line is that the program’s long-run shortfall could be more than $20 trillion higher.

And remember, these numbers are in 2020 dollars. In other words, adjusted for inflation.

So how do we solve this mess? How do we avoid a grim fiscal future?

Shifting to a system of personal retirement accounts would be the most prudent approach. Yes, there would be an enormous transition cost since we would need to pay benefits to current retirees and many older workers, but that transition cost would be less than the $44.7 trillion unfunded liability (or even more!) of the current system.

I’ve written many times about the benefits of personal accounts for the United States, but I find most people are more interested in real-world evidence. Here are just a few of the several dozen nations that either fully or partially utilize private savings instead of political promises.

P.S. Some folks in Washington want to exacerbate Social Security’s fiscal burden by expanding the program.

P.P.S. I hate to add to the bad news, but the long-run finances for Medicare and Medicaid are an even-bigger problem.

No comments:

Post a Comment