Yesterday, the Congressional Budget Office released updated budget projections.

The most important numbers in that report show what’s happening with

the overall fiscal burden of government – measured by both taxes and spending.

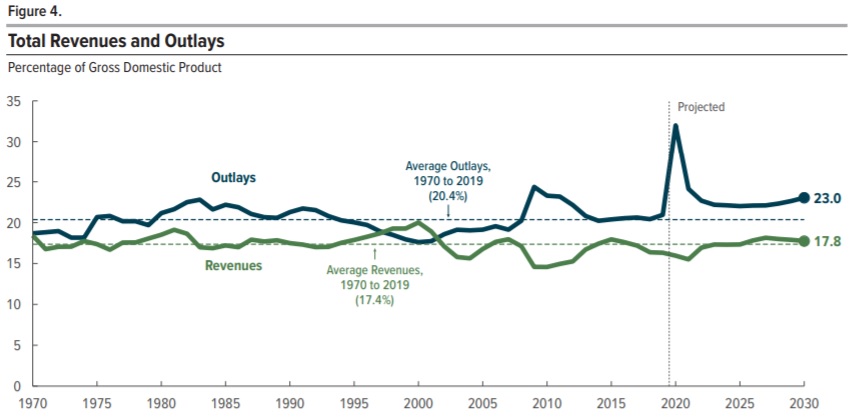

As you can see, there’s a big one-time spike in coronavirus-related spending this year. That’s not good news, but more worrisome is the the longer-run trend of government spending gradually climbing as a share of economic output (and the numbers are significantly worse if you look at CBO’s 30-year projection).

Most reporters and fiscal wonks overlooked the spending data, however, and instead focused on the CBO’s projection for government debt.Since government spending is the problem and borrowing is merely a symptom of that problem, I think it’s a mistake to fixate on red ink. That being said, Figure 3 from the CBO report shows that there’s also an upward-spike in federal debt.

And it is true (remember Greece) that high levels of debt can, by themselves, produce a crisis. This happens when investors suddenly stop buying government bonds because they think there’s a risk of default (which happens when a government is incapable or unwilling to make promised payments to lenders).

I think some nations are on the verge of having that kind of crisis, most notably Italy. But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? In other words, what nations are approaching a tipping point?

A new study from the European Central Bank may help answer these questions. Authored by Pablo Burriel, Cristina Checherita-Westphal, Pascal Jacquinot, Matthias Schön, and Nikolai Stähler, it uses several economic models to measure the downside risks of excessive debt.

That outcome isn’t good for nations with “low” levels of debt, but it can be really bad for nations with “high” debt burdens because they have to deal with much higher interest payments, much bigger tax increases, and much bigger reductions in economic output.

For what it’s worth, I don’t think the study actually gives us any way of determining which nations are near the tipping point. That’s because “low” and “high” are subjective. Japan has an enormous amount of debt, yet investors don’t think there’s any meaningful risk that Japan’s government will default, so it is a “low” debt nation for purposes of the above illustration.

By contrast, there’s a much lower level of debt in Argentina, but investors have almost no trust in that nation’s especially venal politicians, so it’s a “high” debt nation for purposes of this analysis.

The United States, in my humble opinion, is more like Japan. As I wrote last year, “We probably won’t even have a crisis in the next 10 years or 20 years.” And that’s still my view, even after all the spending and debt for coronavirus.

The study concludes with some common-sense advice about using spending restraint and pro-market reforms to create buffers (some people refer to this as “fiscal space“).

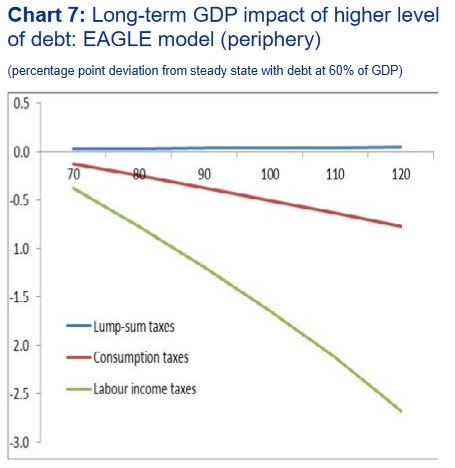

P.S. Here’s another chart from the ECB study that is worth sharing because it confirms that not all tax increases do the same amount of economic damage. We see that consumption taxes (red line) are bad, but income taxes on workers (green line) are even worse.

And if the study included an estimate of what would happen if there were higher income taxes on saving and investment, there would be another line showing even more economic damage.

P.P.S. History shows that nations can reduce very large debt burdens if they follow my Golden Rule.

P.P.P.S. There’s a related study from the IMF that shows how excessive spending is a major warning sign that nations will be vulnerable to fiscal crisis.

As you can see, there’s a big one-time spike in coronavirus-related spending this year. That’s not good news, but more worrisome is the the longer-run trend of government spending gradually climbing as a share of economic output (and the numbers are significantly worse if you look at CBO’s 30-year projection).

Most reporters and fiscal wonks overlooked the spending data, however, and instead focused on the CBO’s projection for government debt.Since government spending is the problem and borrowing is merely a symptom of that problem, I think it’s a mistake to fixate on red ink. That being said, Figure 3 from the CBO report shows that there’s also an upward-spike in federal debt.

And it is true (remember Greece) that high levels of debt can, by themselves, produce a crisis. This happens when investors suddenly stop buying government bonds because they think there’s a risk of default (which happens when a government is incapable or unwilling to make promised payments to lenders).

I think some nations are on the verge of having that kind of crisis, most notably Italy. But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? In other words, what nations are approaching a tipping point?

A new study from the European Central Bank may help answer these questions. Authored by Pablo Burriel, Cristina Checherita-Westphal, Pascal Jacquinot, Matthias Schön, and Nikolai Stähler, it uses several economic models to measure the downside risks of excessive debt.

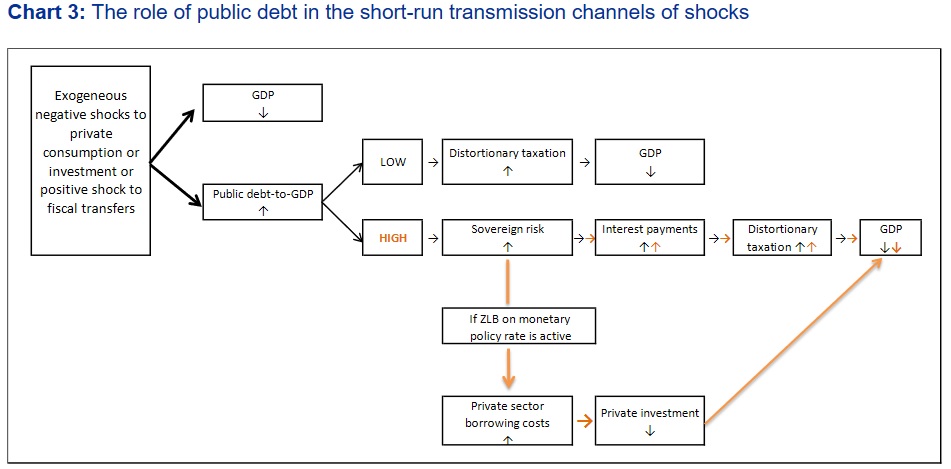

The 2009 global financial and economic crisis left a legacy of historically high levels of public debt in advanced economies, at a scale unseen during modern peace time. …The coronavirus (COVID-19) pandemic is a different type of shock that has dramatically affected global economic activity… Fiscal positions are projected to be strongly hit by the crisis…once the crisis is over and the recovery firmly sets in, keeping public debt at high levels over the medium term is a source of vulnerability… The main objective of this paper is to contribute to the stabilisation vs. sustainability debate in the euro area by reviewing through the lens of large scale DSGE models the economic risks associated with regimes of high public debt.Here’s what they found, none of which should be a surprise.

…we evaluate the economic consequences of high public debt using simulations with three DSGE models… Our DSGE simulations also suggest that high-debt economies…can lose more output in a crisis…have less scope for counter-cyclical fiscal policy and…are adversely affected in terms of potential (long-term) output, with a significant impairment in case of large sovereign risk premia reaction and use of most distortionary type of taxation to finance the additional public debt burden in the future.Here’s a useful chart from the study. It shows some sort of shock on the left (2008 financial crisis or coronavirus being obvious examples), which then produces a recession (lower GDP) and rising debt.

That outcome isn’t good for nations with “low” levels of debt, but it can be really bad for nations with “high” debt burdens because they have to deal with much higher interest payments, much bigger tax increases, and much bigger reductions in economic output.

For what it’s worth, I don’t think the study actually gives us any way of determining which nations are near the tipping point. That’s because “low” and “high” are subjective. Japan has an enormous amount of debt, yet investors don’t think there’s any meaningful risk that Japan’s government will default, so it is a “low” debt nation for purposes of the above illustration.

By contrast, there’s a much lower level of debt in Argentina, but investors have almost no trust in that nation’s especially venal politicians, so it’s a “high” debt nation for purposes of this analysis.

The United States, in my humble opinion, is more like Japan. As I wrote last year, “We probably won’t even have a crisis in the next 10 years or 20 years.” And that’s still my view, even after all the spending and debt for coronavirus.

The study concludes with some common-sense advice about using spending restraint and pro-market reforms to create buffers (some people refer to this as “fiscal space“).

Overall, once the COVID-19 crisis is over and the economic recovery firmly re-established, further efforts to build fiscal buffers in good times and mitigate fiscal risks over the medium term are needed at the national level. Such efforts should be guided by risks to debt sustainability. High debt countries, in particular, should implement a mix of fiscal discipline and wide-ranging growth-enhancing reforms.Needless to say, there’s an obvious and successful way of achieving this goal.

P.S. Here’s another chart from the ECB study that is worth sharing because it confirms that not all tax increases do the same amount of economic damage. We see that consumption taxes (red line) are bad, but income taxes on workers (green line) are even worse.

And if the study included an estimate of what would happen if there were higher income taxes on saving and investment, there would be another line showing even more economic damage.

P.P.S. History shows that nations can reduce very large debt burdens if they follow my Golden Rule.

P.P.P.S. There’s a related study from the IMF that shows how excessive spending is a major warning sign that nations will be vulnerable to fiscal crisis.

No comments:

Post a Comment