When I give speeches on Keynesian economics, I usually begin with a theoretical discussion on why consumer spending is a consequence of growth rather than the cause of growth.

I then focus on two reasons to be skeptical about borrow-and-spend schemes to artificially boost growth.

It is possible, I hypothesize, to increase your short-run consumption if you take money out of a foreigner’s left pocket and put it in your right pocket.

I hasten to add that this is probably not be a wise course of action since the money may be squandered and you simply wind up further in debt, but I admit that the short-run consumption data will be better.

Well, there’s a new academic study on exactly this issue from the European Stability Mechanism (sort of an IMF for eurozone countries).

Here’s what the authors decided to investigate.

And their conclusions, after crunching all the numbers, is that nations can boost short-run consumption if a significant share of new debt is financed by foreigners.

P.S. I feel somewhat guilty for writing a column that acknowledges a potential benefit (albeit transitory and unneighborly) of Keynesian economics, so allow me to expiate my sins by sharing this comparison of Keynesian economics and Austrian economics.

For what it’s worth, I think the Austrians over-emphasize the importance of interest rates. But there’s no question they are much closer to the truth than the Keynesians.

P.P.S. If you want to enjoy some cartoons about Keynesian economics, click here, here, here, and here. Here’s some clever mockery of Keynesianism. And here’s the famous video showing the Keynes v. Hayek rap contest, followed by the equally enjoyable sequel, which features a boxing match between Keynes and Hayek. And even though it’s not the right time of year, here’s the satirical commercial for Keynesian Christmas carols.

I then focus on two reasons to be skeptical about borrow-and-spend schemes to artificially boost growth.

- In the short run, it makes no sense to “stimulate” an economy by borrowing from one group of people and giving the money to another group of people. It’s like trying to become richer by taking money out of your left pocket and putting it in your right pocket.

- In the long run, so-called stimulus creates a ratchet effect for larger government since politicians rarely obey Keynes’ admonition to cut back on government spending and run surpluses when the economy is in an expansion phase.

It is possible, I hypothesize, to increase your short-run consumption if you take money out of a foreigner’s left pocket and put it in your right pocket.

I hasten to add that this is probably not be a wise course of action since the money may be squandered and you simply wind up further in debt, but I admit that the short-run consumption data will be better.

Well, there’s a new academic study on exactly this issue from the European Stability Mechanism (sort of an IMF for eurozone countries).

Here’s what the authors decided to investigate.

Here’s some of the data on foreign holdings of national debt.In this paper, we argue that there is a natural and largely unexplored connection between fiscal multipliers and the foreign holdings of public debt. The intuition is simple….fiscal expansions can…have crowding-out effects on the domestic private sector. Probably the most important among the latter is that the resources used by the domestic private sector to acquire public debt can detract from consumption and investment. This implies that the crowding-out effect of fiscal expansions is likely to be stronger when they are financed by selling public debt to domestic (as opposed to foreign) residents.

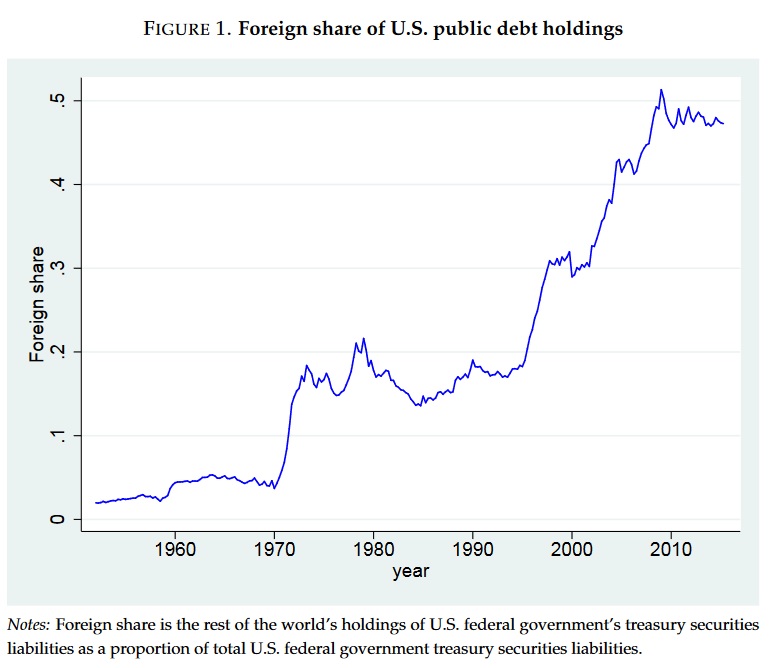

And here’s a chart from the study showing how foreign holdings of U.S. government debt have increased over time.Our data on foreign holdings of public debt reveals interesting patterns. First of all, there is significant variation across countries: in some countries, such as Canada and Japan, the share of public debt held by foreigners is consistently low, whereas in others, such as Finland and Austria, foreigners hold more than 75% of public debt towards the end of the sample. Over time, in line with the rise of financial globalization, the general pattern is one of increasing public debt in the hands of foreigners. In the United States, for instance, the share of public debt held by foreigners has increased from less than 5% in the 1950s to close to 50% today.

And their conclusions, after crunching all the numbers, is that nations can boost short-run consumption if a significant share of new debt is financed by foreigners.

Incidentally, the authors acknowledge that this creates a beggar-thy-neighbor effect.Our main result is that, consistent with the previous argument, the estimated size of fiscal multipliers is increasing in the share of public debt that is in the hands of foreigners. This result holds both for the United States during the postwar period, and for a panel of advanced (OECD) economies over the last few decades. …We find that the average foreign share, i.e., the share of public debt held by foreigners before a fiscal shock, …reflect capital inflows, which help finance fiscal expansions thereby minimizing their crowding-out effects on domestic investment.

Our findings…point to a potentially negative spillover: to the extent that fiscal expansions are financed via foreign borrowing, their crowding-out effects are exported and consumption and investment are reduced elsewhere.

In other words, any transitory benefit one country experiences will be offset by losses elsewhere.

But politicians barely care about their own voters, much less those who live in other countries, so that certainly would not be an effective argument against Keynesian spending binges.

For what it’s worth, I still think the most persuasive argument is that Keynesian economics has an awful track record, even if there’s some ability to shift part of the short-run cost onto foreigners. After all, ask Keynesians to identify an example of successful government stimulus.

And let’s not forget that the long-run costs are always negative because larger government sectors necessarily lead to smaller productive sectors.But politicians barely care about their own voters, much less those who live in other countries, so that certainly would not be an effective argument against Keynesian spending binges.

For what it’s worth, I still think the most persuasive argument is that Keynesian economics has an awful track record, even if there’s some ability to shift part of the short-run cost onto foreigners. After all, ask Keynesians to identify an example of successful government stimulus.

- They certainly can’t pick the big-spending era of Hoover and Roosevelt. That was a flop.

- Japan is another example of Keynesian economics producing debt rather than growth.

- And the Obama stimulus also bombed. Indeed, the unemployment rate didn’t drop until afterwards.

P.S. I feel somewhat guilty for writing a column that acknowledges a potential benefit (albeit transitory and unneighborly) of Keynesian economics, so allow me to expiate my sins by sharing this comparison of Keynesian economics and Austrian economics.

For what it’s worth, I think the Austrians over-emphasize the importance of interest rates. But there’s no question they are much closer to the truth than the Keynesians.

P.P.S. If you want to enjoy some cartoons about Keynesian economics, click here, here, here, and here. Here’s some clever mockery of Keynesianism. And here’s the famous video showing the Keynes v. Hayek rap contest, followed by the equally enjoyable sequel, which features a boxing match between Keynes and Hayek. And even though it’s not the right time of year, here’s the satirical commercial for Keynesian Christmas carols.

No comments:

Post a Comment