October 22, 2020 by Dan Mitchell @ International Liberty

The good news is that the election season is almost over. The bad news is that we’ll have a president next year who does not embrace classical liberal principles of free markets and social tolerance. But that doesn’t mean Trump and Biden are equally bad. Depending on what issues you think are most important, they’re not equally bad in what they say. And, because politicians often make insincere promises, they’re not equally bad in what they’ll actually do.

Regarding Trump, we have a track record. We know he’s pro-market on some issues (taxes and red tape) and we know he’s anti-market on other issues (spending and trade).

Regarding Biden, we have his track record in the United States Senate, where he routinely voted to expand the burden of government. But we also have his presidential platform. And that’s the topic for today’s column. We’re going to review the major economic analyses that have been conducted on his proposals. We’ll start with a report from Moody’s Analytics, authored by Mark Zandi and Bernard Yaros, which compares the economic impacts of the Trump and Biden agendas.

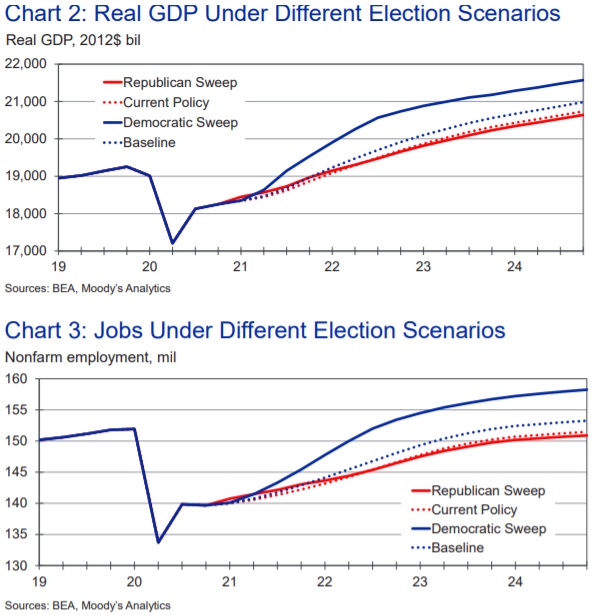

The economic outlook is strongest under the scenario in which Biden and the Democrats sweep Congress and fully adopt their economic agenda. In this scenario, the economy is expected to create 18.6 million jobs during Biden’s term as president, and the economy returns to full employment, with unemployment of just over 4%, by the second half of 2022. During Biden’s presidency, the average American household’s real after-tax income increases by approximately $4,800, and the homeownership rate and house prices increase modestly. Stock prices also rise, but the gains are limited. …Near-term economic growth is lifted by Biden’s aggressive government spending plans, which are deficit-financed in significant part. …Greater government spending adds directly to GDP and jobs, while the higher tax burden has an indirect impact through business investment and the spending and saving behavior of high-income households. …The economic outlook is weakest under the scenario in which Trump and the Republicans sweep Congress and fully adopt their economic agenda. …Trump has proposed much less expansive support to the economy from tax and spending policies.

Here’s the most relevant set of graphs from the report.

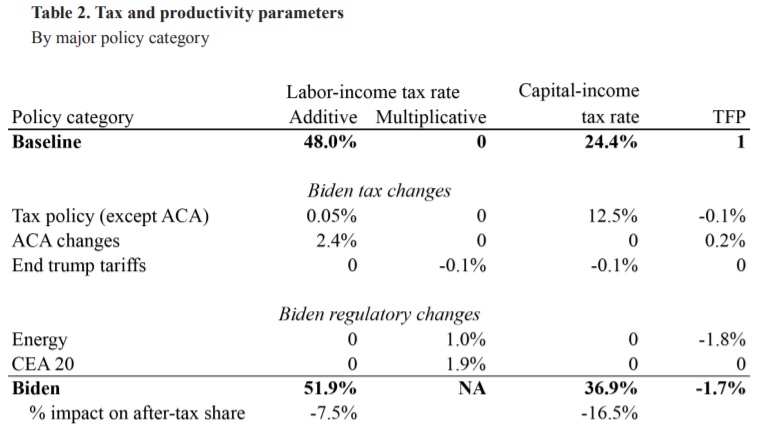

The Moody’s study is an outlier, however. Most other comprehensive analyses are less favorable to Biden. For instance, a study for the Hoover Institution by Timothy Fitzgerald, Kevin Hassett, Cody Kallen, and Casey Mulligan, finds that Biden’s plan will weaken overall economic performance.

We estimate possible effects of Joe Biden’s tax and regulatory agenda. We find that transportation and electricity will require more inputs to produce the same outputs due to ambitious plans to further cut the nation’s carbon emissions, resulting in one or two percent less total factor productivity nationally. Second, we find that proposed changes to regulation as well as to the ACA increase labor wedges. Third, Biden’s agenda increases average marginal tax rates on capital income. Assuming that the supply of capital is elastic in the long run to its after-tax return and that the substitution effect of wages on labor supply is nontrivial, we conclude that, in the long run, Biden’s full agenda reduces fulltime equivalent employment per person by about 3 percent, the capital stock per person by about 15 percent, real GDP per capita by more than 8 percent, and real consumption per household by about 7 percent.

Wonkier readers may be interested in these numbers, which show that there’s a modest benefit from unwinding some of Trump’s protectionism, but there’s a lot of damage from the the other changes proposed by the former Vice President.

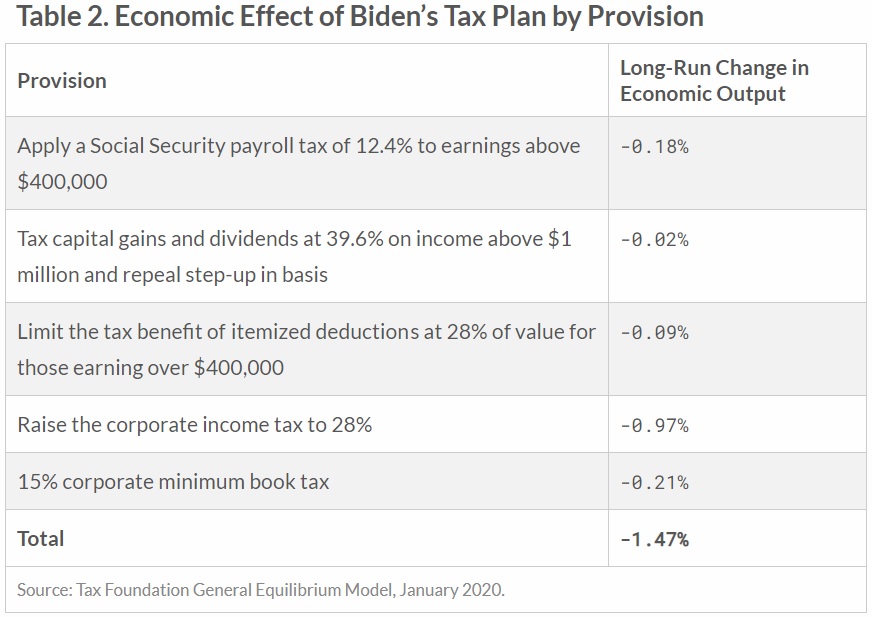

In a report authored by Garrett Watson, Huaqun Li, and Taylor LaJoie, the Tax Foundation estimated the impact of Biden’s proposed policies. Here are some of the highlights.

According to the Tax Foundation General Equilibrium Model, Biden’s tax plan would reduce the economy’s size by 1.47 percent in the long run. The plan would shrink the capital stock by just over 2.5 percent and reduce the overall wage rate by a little over 1 percent, leading to about 518,000 fewer full-time equivalent jobs. …Biden’s tax plan would raise about $3.05 trillion over the next decade on a conventional basis, and $2.65 trillion after accounting for the reduction in the size of the U.S. economy. While taxpayers in the bottom four quintiles would see an increase in after-tax incomes in 2021 primarily due to the temporary CTC expansion, by 2030 the plan would lead to lower after-tax income for all income levels.

Table 2 from the report is worth sharing because it shows what policies have the biggest economic impact.

The bottom line is that it’s not a good idea to raise the corporate tax burden and it’s not a good idea to worsen the payroll tax burden. Here are some excerpts by a study authored by Professor Laurence Kotlikoff for the Goodman Institute.

The micro analysis is based on The Fiscal Analyzer (TFA), which uses data from the Federal Reserve’s Survey of Consumer Finance to calculate how much representative American households will pay in taxes net of what they will receive in benefits over the rest of their lives. …The key micro issues…are the degree to which the Vice President’s reforms alter relative remaining lifetime net tax burdens and lifetime spending of the rich and poor within specific age cohorts and the impact of the reforms on incentives to work, i.e., remaining lifetime marginal net tax rates. The macro analysis is based on the Global Gaidar Model (GGM)…a dynamic, 90-period OLG, 17-region general equilibrium model. …The analysis includes three sets of findings. The first is the change in lifetime net taxes defined as the change in lifetime net taxes. The second is the percentage change in lifetime spending, defined as the change in the present value of outlays on all goods and services as well as bequests, averaged across all survivor path. The third is the lifetime marginal net tax rate from earning an extra $1,000. TFA’s lifetime marginal net tax rate measure takes full account of so-called double taxation. …The GGM predicts a close to 6 percent reduction in the U.S. capital stock. The GGM predicts close to a 2 percent permanent reduction in annual U.S. GDP. The GGM predicts a roughly 2 percentage-point reduction in wages of U.S. workers, with a larger reduction in the wages of high-skilled workers.

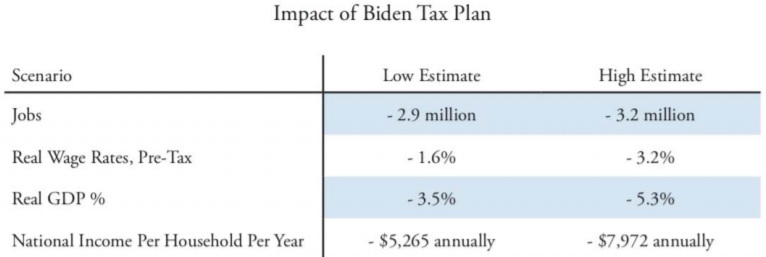

In a study for the Committee to Unleash Prosperity, Professor Casey Mulligan estimated the following effects.

This study addresses the impact of these tax rate changes on economic behavior – work, investment, output and growth. This study finds that the Biden tax agenda will reduce production, incomes, and employment per capita by increasing taxation of both labor and business capital. Employment will be about 3 million workers less in the long run (five to ten years). This employment effect is primarily due to the agenda’s expansion of health insurance credits, which raises the average marginal tax rates on labor income by 2.4 percentage points. Biden also plans to increase taxes on businesses and their owners by a combined 6 to 10 percentage points. These taxes will reduce long-run wages, GDP per worker, and business capital per worker in the long run. By decreasing both the number of workers per capita and GDP per worker, respectively, these two key elements of Biden’s agenda reinforce to significantly reduce GDP per capita and average household incomes. I estimate that, as a result of Biden’s tax agenda, real GDP per capita would be 4 to 5 percent less, which is about $8,000 per household per year in the long run. The two parts of the tax agenda combine to reduce real per capita business capital by 7 to 12 percent in the long run.

Here’s a table from the study.

I’ll add two points to the above analyses.

First, the reason that the Moody’s study produces wildly different results is that its model is based on Keynesian principles. As such, a bigger burden of government spending is assumed to stimulate growth.

For what it’s worth, I think borrowing and spending can lead to short-run increases in consumption, but I’m very skeptical that Keynesian policies can generate increases in national income (i.e., what we produce rather than what we consume) over the medium-run or long-run.

All of the other studies rely on models that estimate how government policies impact incentives to engage in productive behavior. They don’t all measure the same things (some of the studies look solely at taxes, some look at overall fiscal policy, and some also include a look at regulatory proposals) but the methodologies are similar.

Second, I’ll re-emphasize the point I made at the beginning about how politicians routinely say things during campaigns that are either insincere or impractical.

For instance, Trump promised to restrain domestic discretionary spending by $750 billion and he actually increased it by $700 billion.

Likewise, I don’t expect Biden (assuming he prevails) to deliver on his campaign promises. In this case, that’s good news since he won’t increase taxes and spending by nearly as much as what he’s embraced during the campaign (in my fantasy world, he turns out be like Bill Clinton and actually delivers a net reduction in the burden of government).

P.S. For those on the losing side of the upcoming election, I’ll remind you that Australia is probably the best option if you want to escape the United States. Though you may want to pick Switzerland if you have a lot of money.

No comments:

Post a Comment