Speculating about tax policy in 2021, with Washington potentially being controlling by Joe Biden, Chuck Schumer, and Nancy Pelosi, there are four points to consider.

- The bad news is that Joe Biden has endorsed a wide range of punitive tax increases.

- The good news is that Joe Biden has not endorsed a wealth tax, which is one of the most damaging ways – on a per-dollar raised basis – for Washington to collect more revenue.

- The worse news is that the additional spending desired by Democrats is much greater than Biden’s proposed tax increases, which means there will be significant pressures for additional sources of money.

- The worst news is that the class-warfare mentality on the left means the additional tax increases will target successful entrepreneurs, investors, innovators, and business owners – which means a wealth tax is a very real threat.

They based their analysis on the plan proposed by Senator Elizabeth Warren, which is probably the most realistic option since Biden (assuming he wins the election) presumably won’t choose the more radical plan proposed by Senator Bernie Sanders. They have a sophisticated model of the U.S. economy. Here’s their simplified description of how a wealth tax would harm incentives for productive behavior.

The most direct effect operates through the reduction in wealth of the affected taxpayers, including the reduction in accumulated wealth over time. Although such a reduction in wealth is, for at least some proponents of the wealth tax, a desirable result, the associated reduction in investment and thus in the capital stock over time will have deleterious effects, reducing labor productivity and thus wage income as well as economic output. …A wealth tax would also affect saving by changing the relative prices of current and future consumption. In the standard life-cycle model of household saving, a wealth tax effectively increases the price of future consumption by lowering the after-tax return to saving, creating a tax bias favoring current consumption and thus reducing saving. … we should note that the apparently low tax rates under the typical wealth tax are misleading if they are compared to income tax rates imposed on capital income, and the capital income tax rates that are analogous to wealth tax rates are often in excess of 100 percent. …For example, with a 1 percent wealth tax and a Treasury bond earning 2 percent, the effective income tax rate associated with the wealth tax is 50 percent; with a 2 percent tax rate, the effective income tax rate increases to 100 percent.And here are the empirical findings from the report.

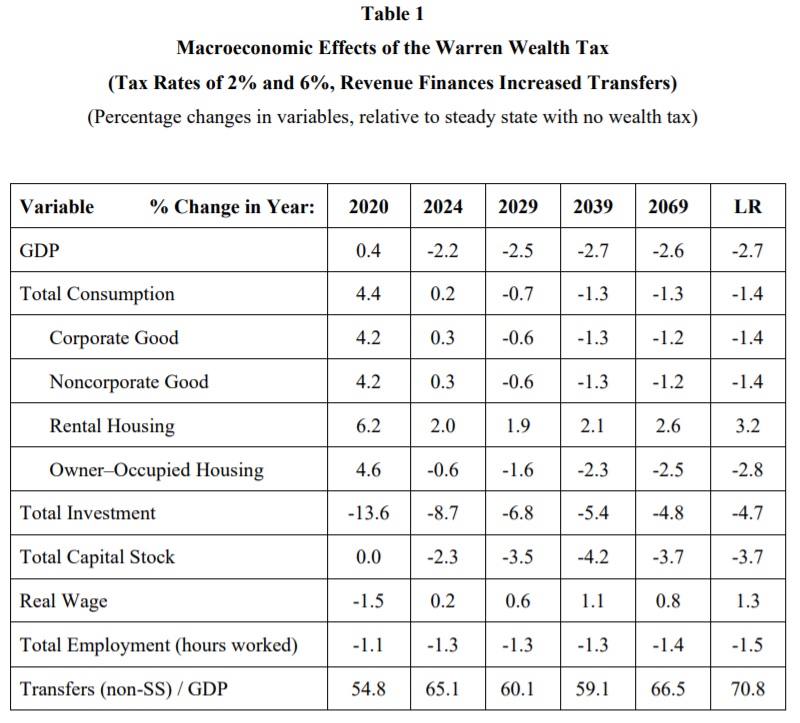

We compare the macroeconomic effects of the policy change to the values that would have occurred in the absence of any changes — that is, under a current law long run scenario… The macroeconomic effects of the wealth tax are shown in Table 1. Because the wealth tax reduces the after-tax return to saving and investment and increases the cost of capital to firms, it reduces saving and investment and, over time, reduces the capital stock. Investment declines initially by 13.6 percent…and declines by 4.7 percent in the long run. The total capital stock declines gradually to a level 3.5 percent lower ten years after enactment and 3.7 percent lower in the long run… The smaller capital stock results in decreased labor productivity… The demand for labor falls as the capital stock declines, and the supply of labor falls as households receive larger transfer payments financed by the wealth tax revenues… Hours worked decrease initially by 1.1 percent and decline by 1.5 percent in the long run. …the initial decline in hours worked of 1.1 percent would be equivalent to a decline in employment of approximately 1.8 million jobs initially. The declines in the capital stock and labor supply imply that GDP declines as well, by 2.2 percent 5 years after enactment and by 2.7 percent in the long run.Here’s the table mentioned in the above excerpt. At the risk of understatement, these are not favorable results.

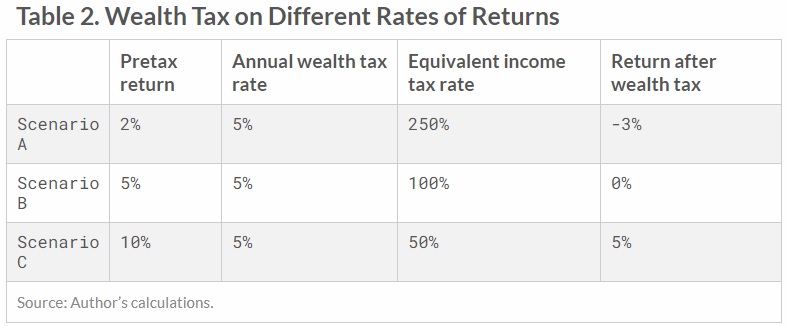

Other detailed studies on wealth taxation also find very negative results. The Tax Foundation’s study, authored by Huaqun Li and Karl Smith, also is worth perusing. For purposes of today’s analysis, I’ll simply share one of the tables from the report, which echoes the point about how “low” rates of wealth taxation actually result in very high tax rates on saving and investment.

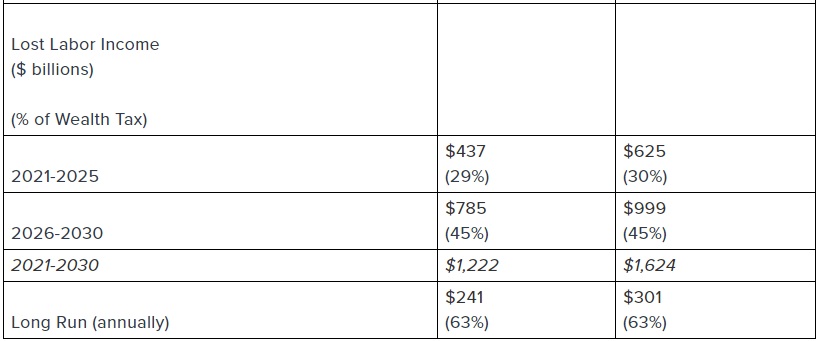

The American Action Forum also released a study. Authored by Douglas Holtz-Eakin and Gordon Gray, it’s filled with helpful information. The part that deserves the most attention is this table showing how a wealth tax on the rich results in lost wages for everyone else.

Yes, the rich definitely lose out because their net wealth decreases. But presumably the rest of us are more concerned about the fact that lower levels of saving and investment reduce labor income for ordinary people. The bottom line is that wealth taxes are very misguided, assuming the goal is a prosperous and competitive America.

P.S. One obvious effect of wealth taxation, which is mentioned in the study from the Center for Freedom and Prosperity, is that some rich people will become tax expatriates and move to jurisdictions (not just places such as Monaco, Bermuda, or the Cayman Islands, but any of the other 200-plus nations don’t tax wealth) where politicians don’t engage in class warfare.

No comments:

Post a Comment