There will be many lessons that we hopefully learn from the current crisis, most notably that it’s foolish to give so much regulatory power to sloth-like bureaucracies such as the FDA and CDC.

Today, I want to focus on a longer-run lesson, which is how tax policy (a bias for debt over equity) and monetary policy (artificially low interest rates) encourage excessive private debt.

Are current debt levels excessive? Let’s look at some excerpts from a column in the Washington Post, which was written by David Lynch last November – before coronavirus started wreaking havoc with the economy.

Little more than a decade after consumers binged on inexpensive mortgages that helped bring on a global financial crisis, a new debt surge — this time by major corporations — threatens to unleash fresh turmoil. A decade of historically low interest rates has allowed companies to sell record amounts of bonds to investors, sending total U.S. corporate debt to nearly $10 trillion… Some of America’s best-known companies…have splurged on borrowed cash. This year, the weakest firms have accounted for most of the growth and are increasingly using debt for “financial risk-taking,”… “We are sitting on the top of an unexploded bomb, and we really don’t know what will trigger the explosion,” said Emre Tiftik, a debt specialist at the Institute of International Finance, an industry association. …The root cause of the debt boom is the decision by the Federal Reserve and other key central banks to cut interest rates to zero in the wake of the financial crisis and to hold them at historic lows for years.

Now we have coronavirus, and George Melloan explained a few days ago in the Wall Street Journal that the “unexploded bomb” has detonated.

Melloan’s final points deserve emphasis. There are good reasons to reconsider the Federal Reserve, and we definitely should be angry about the perverse redistribution enabled by Fed policies.The Covid-19 pandemic…will do further damage to the global economy… The danger is heightened by the heavy load of debt American corporations have piled up as they have taken advantage of low-cost borrowing. …Cheap credit brought on the heavy overload of corporate debt. The Federal Reserve has responded to the virus by—what else?—making credit even cheaper, cutting its fed funds lending rate all the way to 0%-0.25% on Sunday. …Rate cuts in response to crises are programmed into the Fed’s software. There is no compelling evidence that they are a solution or even a remedy. …the low interest rates of the past decade have ballooned all forms of debt: government, consumer, corporate. Corporate debt, the most worrisome type at the moment, stands at about $10 trillion and has made a steady climb to 47% of gross domestic product, a record level… But even cheap borrowing and securitized debt obligations have to be paid back. It becomes harder to make payments when a global health crisis is killing sales and your company is bleeding red ink. …the increased political bias toward easy money remains a problem. The Federal Reserve Act of 1913 was political from the day Woodrow Wilson signed it. It has gotten more political ever since, increasingly becoming an instrument for robbing the poor—savers and pensioners—and giving to often profligate borrowers.

But let’s keep our focus on the topic of government-encouraged debt and how it contributes to economic instability.

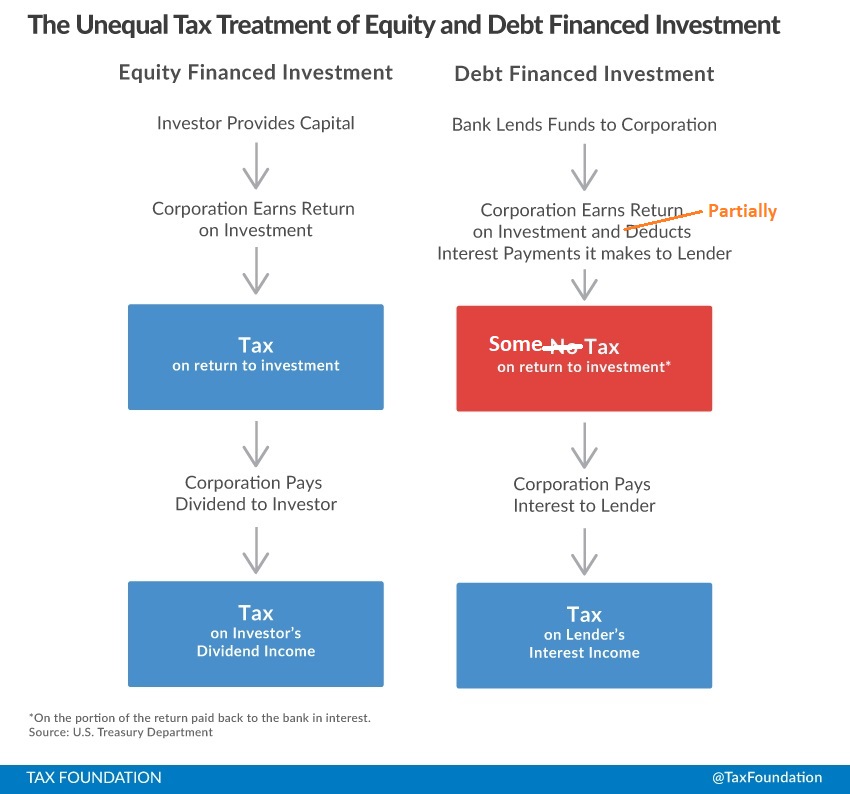

It’s not just an issue of bad monetary policy. We also have a tax code that encourages companies to disproportionately utilize debt.

But the 2017 tax bill addressed that flaw, as Reihan Salam explained two years ago in an article for National Review.

That’s the good news (along with the lower corporate rate and restriction on deductibility of state and local taxes).…one of the TCJA’s good points…limits that the legislation places on corporate interest deductibility, which…could change the way companies in the United States do business and make the U.S. economy more stable. …By stipulating that companies cannot use the interest deduction to reduce their earnings by more than 30 percent, the law made taking on debt somewhat less attractive compared to seeking financing by offering equity to investors. …equity is more flexible in times of crisis than debt, which means that problems are less likely to spiral out of control.

The bad news is that the 2017 law only partially addressed the bias for debt over equity. Companies still have a tax-driven incentive to prefer borrowing.

Here’s the Tax Foundation’s depiction of how the pre-TCJA system worked, which I’ve altered to show how the new system operates.

I’ll close with the observation that there’s nothing necessarily wrong with private debt. Families borrow to buy homes, for instance, and companies borrow for reasons such as financing research and building factories.

But debt only makes sense if it’s based on market-driven factors (i.e., will borrowing enable future benefits and will there be enough cash to make payments). And that includes planning for what happens if there’s a recession and income falls.

Unfortunately, government intervention has distorted market signals and the result is excessive debt. And now the economic damage of the coronavirus will be even higher because more companies will become insolvent.

P.S. Even the International Monetary Fund is on the correct side about the downsides of tax-driven debt.

P.P.S. In addition to eliminating the bias for debt over equity, it also would be a very good idea to get rid of the bias for current consumption over future consumption (i.e., double taxation).

No comments:

Post a Comment