The coronavirus is a genuine threat to prosperity, at least in

the short run, in large part because it is causing a contraction in

global trade.

The silver lining to that dark cloud is that President Trump may learn that trade is actually good rather than bad.

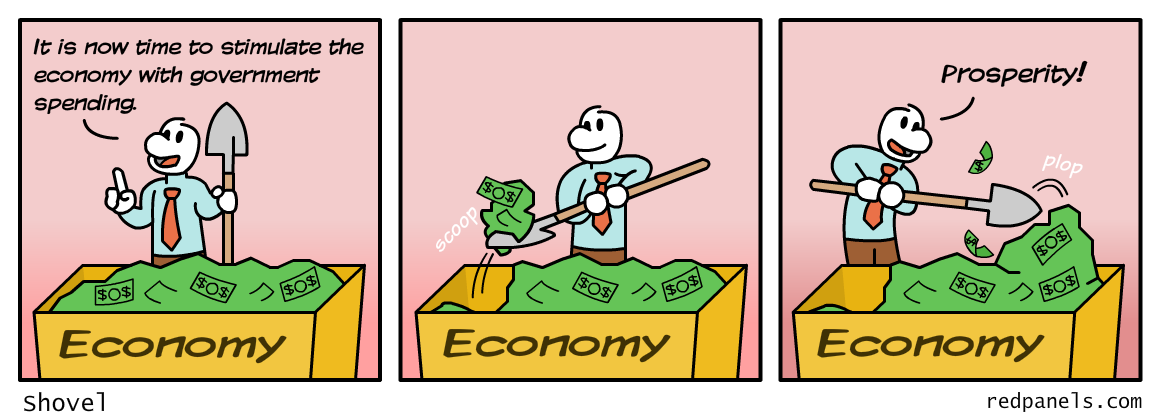

But dark clouds also can have dark linings, at least when the crowd in Washington decides it’s time for another dose of Keynesian economics.

- Fiscal Keynesianism – the government borrows money from credit markets and politicians then redistribute the funds in hopes that recipients will spend more.

- Monetary Keynesianism – the government creates more money in hopes that lower interest rates will stimulate borrowing and recipients will spend more.

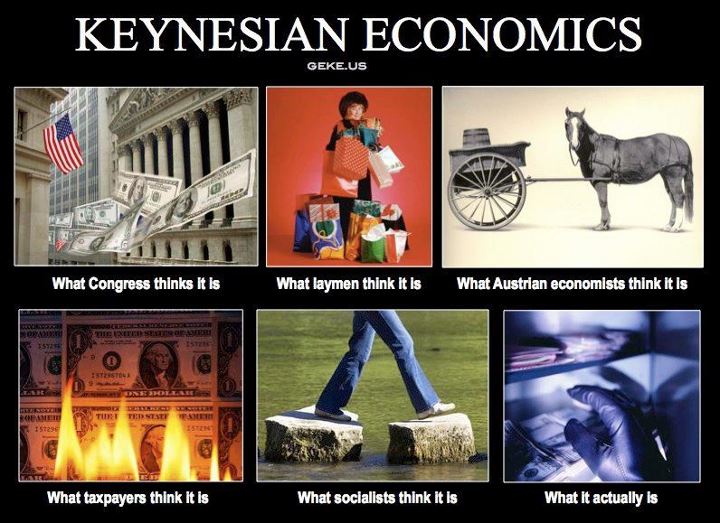

Critics warn, correctly, that Keynesian policies are misguided. More spending is a consequence of economic growth, not the trigger for economic growth. But the “bad penny” of Keynesian economics keeps reappearing because it gives politicians an excuse to buy votes.

The Wall Street Journal opined this morning about the risks of more Keynesian monetary stimulus.

The Federal Reserve has become the default doctor for whatever ails the U.S. economy, and on Tuesday the financial physician applied what it hopes will be monetary balm for the economic damage from the coronavirus. …The theory behind the rate cut appears to be that aggressive action is the best way to send a strong message of economic insurance. …Count us skeptical. …Nobody is going to take that flight to Tokyo because the Fed is suddenly paying less on excess reserves. …The Fed’s great mistake after 9/11 was that it kept rates at or near 1% for far too long even after the 2003 tax cut had the economy humming. The seeds of the housing boom and bust were sown.And the editorial also warned about more Keynesian fiscal stimulus.

Even if a temporary tax cuts is the vehicle used to dump money into the economy.

This being an election year, the political class is also starting to demand more fiscal “stimulus.” …If Mr. Trump falls for that, he’d be embracing Joe Bidenomics. We tried the temporary payroll-tax cut idea in the slow growth Obama era, reducing the worker portion of the levy to 4.2% from 6.2% of salary. It took effect in January 2011, but the unemployment rate stayed above 9% for most of the rest of that year. Temporary tax cuts put more money in peoples’ pockets and can give a short-term lift to the GDP statistics. But the growth effect quickly vanishes because it doesn’t permanently change the incentive to save and invest.Excellent points.

Permanent supply-side tax cuts encourage more prosperity, not temporary Keynesian-style tax cuts.

Given the political division in Washington, it’s unclear whether politicians will agree on how to pursue fiscal Keynesianism.

But that doesn’t mean we can rest easy. Trump is a fan of Keynesian monetary policy and the Federal Reserve is susceptible to political pressure.

Just don’t expect good results from monetary tinkering. George Melloan wrote about the ineffectiveness of monetary stimulus last year, well before coronavirus became an issue.

The most recent promoters of monetary “stimulus” were Barack Obama and the Fed chairmen who served during his presidency, Ben Bernanke and Janet Yellen. …the Obama-era chairmen tried to stimulate growth “by keeping its policy rate at zero for six-and-a-half years into the economic recovery and more than quadrupled the size of the Fed’s balance sheet.” And what do we have to show for it? After the 2009 slump, economic growth from 2010-17 averaged 2.2%, well below the 3% historical average, despite the Fed’s drastic measures. Low interest rates certainly stimulate borrowing, but that isn’t the same as economic growth. Indeed it can often restrain growth. …Congress got the idea that credit somehow comes free of charge. So now the likes of Elizabeth Warren and Bernie Sanders think there is no limit to how much Uncle Sam can borrow. Easy money not only expands debt-service costs but also encourages malinvestment. …when Donald Trump hammers on the Fed for lower rates, …he is embarked on a fool’s errand.Since the Federal Reserve has already slashed interest rates, that Keynesian horse already has left the barn.

That being said, don’t expect positive results. Keynesian economics has a very poor track record (if fiscal Keynesianism and monetary Keynesianism were a recipe for success, Japan would be booming).

So let’s hope politicians don’t put a saddle on the Keynesian fiscal horse as well.

If Trump really feels he has to do something, I ranked his options last summer.

The bottom line is that good short-run policy is also good long-run policy.

No comments:

Post a Comment