Most people (though not all) understand that inflation is the result of bad monetary policy.

That’s the easy part to grasp.

What’s more difficult is figuring out why politicians and their central bankers impose bad monetary policy.

- Are they creating too much money because they want to artificially goose the economy with Keynesian monetary policy, especially during election season?

- Are they creating too much money because they want to finance more government spending with modern monetary theory, like Turkey, Argentina, or Sri Lanka?

My rule of thumb has been that developed nations make Mistake #1 and developing nations make Mistake #2.

But that may be changing because of irresponsible fiscal policy in richer nations.

For instance, the European Central Bank has been propping up Italy, financing a big chunk of that nation’s deficit spending.

And I worry something similar may be happening the United States.

The incentive doesn’t even require a belief in a nutty idea like Modern Monetary Theory. Government can profit from inflation in a more subtle way, as I wrote way back in 2011.

Let’s expand on that column, thanks to a a new study from the International Monetary Fund.

Authored by Daniel Garcia-Macia, it crunches a bunch of data to develop estimates of how governments benefit from unexpected inflation.

This paper has shown that inflation surprises help to reduce deficits temporarily and debt ratios persistently. Deficit-to-GDP ratios decline as the nominal values of the economy’s output and of tax bases generally rise, generating more revenues. …an unexpected bout of inflation will erode part of the real value of government debt persistently, both owing to the initial improvement in fiscal balances and the nominal GDP denominator effect. …Unexpected inflation may offer some breathing room for debt ratios but attempts to keep surprising markets and economic agents have historically proven futile or harmful. …Another important dimension is which budget items are automatically or de facto indexed for inflation and by which mechanism.

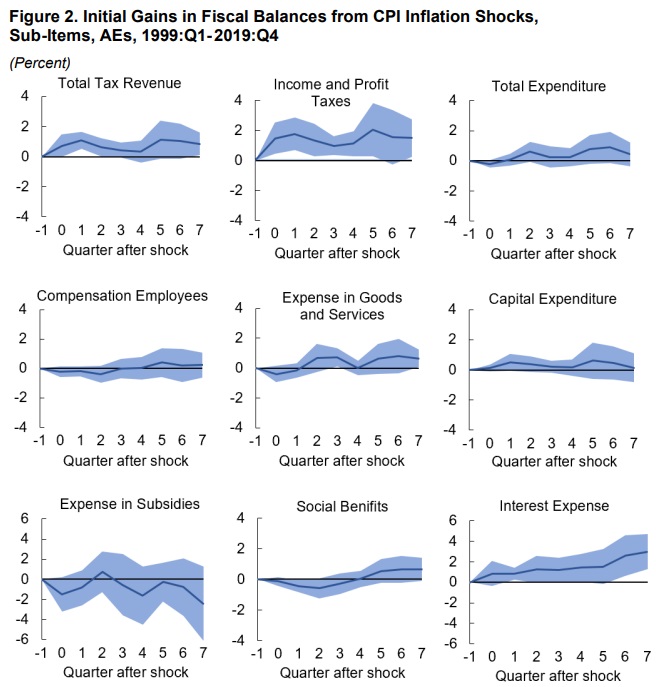

Here’s a look at different fiscal variables and how unexpected inflation during a two-year period.

What politicians presumably care about are the first two charts on the first row. You can see that inflation leads to more tax revenue, especially from taxes on income and profits.

I fear that they are less concerned (if at all) about the fact that inflation is bad for taxpayers and bad for the economy.

Sadly, there’s not much people can do to protect themselves from inflation. Unless, of course, we figure out an alternative to central banks.

Central Banks, Politicians, and Inflation: Part II

October 28, 2023 by Dan Mitchell

I wrote yesterday about the two big reasons that central banks – such as the Federal Reserve in Washington – impose misguided monetary policy.

|

- They create too much money because they want to artificially goose the economy with Keynesian monetary policy, especially during election season.

- They create too much money because they want to finance more government spending based on the nutty idea of modern monetary theory (an approach that has failed in places like Turkey, Argentina, or Sri Lanka).

In Part II, let’s consider whether there are ways to block or discourage irresponsible monetary policy.

For hard-core libertarians, the answer is easy. Just abolish the Fed and rely on the private sector to produce competing currencies.

That approach actually used to exist in some nations in the 1800s and earlier, and it has a good track record.

< <

|

Another option is a gold standard.

That approach to exist before World War I and also has a good track record.

But it’s also not terrible realistic, especially since there are good reasons to think governments today wouldn’t implement and maintain it in a sensible manner.

So most proponents of good policy today focus on more targeted reforms, most of which are designed to discourage central bankers from imposing inflationary policy.

But not everyone favors anti-inflation policies. In an editorial about various GOP economic proposals, the Washington Post criticizes any limits on the powers of the Federal Reserve.

Even worse is the rising urge to attack the Federal Reserve. While in office, Mr. Trump mused publicly about firing Fed Chair Jerome H. Powell. Entrepreneur Vivek Ramaswamy wants to restrict the Fed’s mandate to “stabilize the dollar & nothing more.”

Mr. Pence wants to end the Fed’s dual mandate — minimizing inflation and maximizing employment — in favor of an inflation-fighting-only mission. Mr. DeSantis vows to “rein in” the Fed and stop its development of a digital currency. Since the early 20th century, Fed independence has undergirded U.S. prosperity; meddling with the central bank would cause immediate and immense economic harm.

The editorial is wrong. If you want to know whether the Fed has “undergirded U.S. prosperity,” just watch this video and you’ll quickly learn the Fed has been a destabilizing force, producing boom-bust cycles (and the busts are always worse than the booms).

Regarding some of the specific ideas cited in the editorial, Pence and Ramaswamy are right to say that the Fed should focus solely on price stability, which is just another way of saying we should not have Keynesian monetary policy.

And kudos to DeSantis for opposing a central bank digital currency. Governments would have vast new powers to abuse if cash was eliminated.

P.S. If you want some Fed humor, we have a Who-is-Ben-Bernanke t-shirt, this Fed song parody, some special Federal Reserve toilet paper, Ben Bernanke’s hacked Facebook page, and the famous “Ben Bernank” video.

No comments:

Post a Comment