In the world of fiscal policy, there are actually two big debates.

- One debate revolves around the appropriate size of government in the long run. Folks on the left argue that government spending generates a lot of value and that bigger government is a recipe for more prosperity. Libertarians and their allies, by contrast, point out that most forms of government spending are counterproductive and that large public sectors (and the accompanying taxes) undermine economic performance.

- The other debate is focused on short-run economic effects, and revolves around the

- “Keynesian” argument that more government spending is a “stimulus” to a weak economy and that budget-cutting “austerity” hurts growth. Libertarians and other critics are generally skeptical that government spending boosts short-run growth and instead argue that the right kind of austerity (i.e., a lower burden of government spending) is the appropriate approach.

Back in 2009 and 2010, I wrote a lot about the Keynesian stimulus fight. In more recent years, however, I have focused more on the debate over the growth-maximizing size of government.

Back in 2009 and 2010, I wrote a lot about the Keynesian stimulus fight. In more recent years, however, I have focused more on the debate over the growth-maximizing size of government.But it’s time to revisit the stimulus/austerity debate. The National Bureau of Economic Research last month released a new study by five economists (two from Harvard, one from NYU, and two from Italian universities) reviewing the real-world evidence on fiscal consolidation (i.e., reducing red ink) over the past several decades.

This paper studies whether what matters most is the “when” (whether an adjustment is carried out during an expansion, or a recession) or the “how” (i.e. the composition of the adjustment, whether it is mostly based on tax increases, or on spending cuts). …We estimate a model which allows for both sources of non-linearity: “when” and “how”.Here’s a bit more about the methodology.

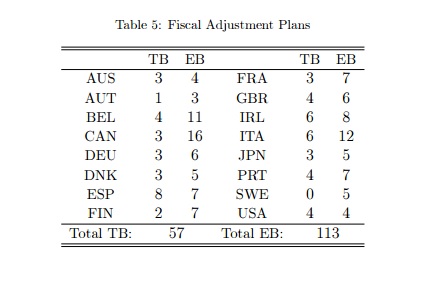

The fiscal consolidations we study are those implemented by 16 OECD countries (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Portugal, Spain, Sweden, United Kingdom, United States) between 1981 and 2014. …We also decompose each adjustment in its two components: changes in taxes and in spending. …we use a specification in which the economy, following the shift in fiscal policy, can move from one state to another. We also allow multipliers to vary depending on the type of consolidation, tax-based vs expenditure-based. …Our government expenditure variable is total government spending net of interest payments on the debt: that is we do not distinguish between government consumption, government investment, transfers (social security benefits etc) and other government outlays. …In total we have 170 plans and 216 episodes, of which about two-thirds are EB and one-third are TB.By the way, “EB” refers to “expenditure based” fiscal consolidations and “TB” refers to “tax based” consolidations.

And you can see from Table 5 that some countries focused more on tax increases and others were more focused on trying to restrain spending.

And you can see from Table 5 that some countries focused more on tax increases and others were more focused on trying to restrain spending.Congratulations to Canada and Sweden for mostly or totally eschewing tax hikes.

Though I wonder how many of the 113 “EB” plans involved genuine spending reforms (probably very few based on this data) and how many were based on the fake-spending-cuts approach that is common in the United States.

But I’m digressing.

Let’s now look at some findings from the NBER study, starting with the fact that most consolidations took place during downturns, which certainly wouldn’t please Keynesians, but shouldn’t be too surprising since red ink tend to rise during such periods.

…there is a relation between the timing and the type of fiscal adjustment and the state of the economy. Overall, adjustment plans are much more likely to be introduced during a recession. There was a consolidation in 62 out of 99 years of recession…, while we record a consolidation in only 13 over 94 years of expansion. …it is somewhat surprising that a majority of the shifts in fiscal policy devoted to reducing deficits are implemented during recessions.And here are the results that really matter. The economists crunched the numbers and found that tax increases impose considerable damage, whereas spending cuts cause very little harm to short-run performance.

We find that the composition of fiscal adjustments is more important than the state of the cycle in determining their effect on output. Fiscal adjustments based upon spending cuts are much less costly in terms of short run output losses – such losses are in fact on average close to zero – than those based upon tax increases which are associated with large and prolonged recessions regardless of whether the adjustment starts in a recession or not. …what matters for the short run output cost of fiscal consolidations is the composition of the adjustment. Tax-based adjustments are costly in terms of output losses. Expenditure-based ones have on average very low costs.These findings are remarkable. Even I’m willing to accept that spending cuts may be painful in the short run (not because of Keynesian reasons, but simply because resources don’t instantaneously get reallocated to more productive uses).

So if the economists who wrote this comprehensive study find that there is very little short-run dislocation associated with spending cuts, that’s powerful evidence.

And when you then consider all the data and research showing the positive long-run effects of smaller government, this certainly suggests that the top fiscal priority should be shrinking the size and scope of government.

P.S. I mentioned above that Keynesians doubtlessly get agitated that governments engage in fiscal consolidation during downturns. This is why I’m trying to get them to support spending caps. The good news, from their perspective, is that the government’s budget would be allowed to grow when there’s a recession, albeit not very rapidly. The tradeoff that they must accept, however, is that spending would be limited to that modest growth rate even during years when there’s strong growth and the private sector is generating lots of tax revenue.

Honest Keynesians presumably should yes to this deal since Keynes wanted restraint during growth years to offset “stimulus” during recession years. And economists at left-leaning international bureaucracies seem sympathetic to this tradeoff. I don’t think there are many honest Keynesians in the political world, however, so I’m not expecting to get a lot of support from my leftist friends in Washington.

No comments:

Post a Comment